What States Can Do to Improve Health Savings Account Incentives

on a table.")

Author

Byron Schlomach

Abstract

This paper explains how HSA incentives (meant to battle the third-party payer problem) are undermined by insurance companies. It proposes actions states can take, including requiring insurance companies to count self-pay claims toward a consumer’s deductible. It also recommends that the federal government liberalize HSA policy in order to revolutionize how health care is financed.

Full Text HTML

What States Can Do to Improve Health Savings Account Incentives

Byron Schlomach

Health Savings Accounts (HSAs) are personal savings accounts whose deposits from their owner’s current income and from which the owner can spend funds on certain medical expenses without income tax repercussions. Income diverted by an individual to an HSA is not taxed. Interest or other earnings that accrue to an HSA are not taxed. Withdrawals to pay for medical expenses defined under federal law are not taxed. Annual HSA contributions are only allowed up to certain amounts (currently $3,600 for an individual and $7,200 for a family[1]). Contributions may be made by HSA owners or by employers on behalf of individual employees and/or their families. HSA contributions can only be made if an individual is covered by a high deductible health insurance plan (minimum $1,400 deductible for a person, $2,800/family; maximum out-of-pocket $7,000/single, $14,000/family[2]). Although there are yearly contribution limits, balances may accumulate. On retirement, an HSA owner may make withdrawals to spend for non-healthcare purposes without tax penalty, but must pay tax on such withdrawals as income.

As of January 2020, HSA assets stood at almost $72 billion.[3] As large as this sum might sound, it is paltry (less than two percent) when compared to the $3.8 trillion spent on health care in 2019 alone.[4] HSA accumulation would be greater were it not for the fact that so many Americans regularly spend nearly all of their yearly contributions.[5] One reason Americans quickly spend down their HSA balances is related to how HSA-financed purchases are treated by insurance companies for deductible purposes. As explained in more detail below, if an individual with a high deductible health plan pays cash to a provider without recourse to insurance, that purchase will likely not be counted toward their deductible. Consequently, HSA account holders pay out of their HSAs as insured customers and lose out on substantial cash-pay discounts since they are charged the price agreed to by their insurance company.

Health Savings Accounts are intended to make consumers of health care act like consumers in other markets and incentivize them to question medical billing and practices in order to preserve personal wealth. Given that someone can only take advantage of an HSA in conjunction with a high deductible health plan, an HSA does not exactly turn an account holder into a cash payer. Nevertheless, the intent is to begin re-creating a true market in health care by incentivizing patients to push back on providers by asking questions about the cost and need of recommended procedures, hopefully by shopping around for better prices given that most medical services are not rendered in the context of an emergency.[6]

Health Care’s Third-Party Payer Problem

Any time a person consumes something someone else is paying for, it is natural for that person to view that something as free. Of course, nothing is truly free, but under the circumstances of someone else paying, and especially if the consumer has no idea of the cost of something paid for by a third party, the consumer does not feel constrained and consumes freely. For example, public education suffers from this phenomenon. Parents who send their children to public schools bear only a fraction of the cost through property taxes, but have no idea what the total cost is. They often demand services they view as education related without any thought to the cost of what they demand.

In health care, there are two major third-party payers – government and employer-paid health insurers. Only 10 percent of health care expenditures are paid directly from patients’ pockets. The bulk of healthcare spending occurs through the federal Medicare/Medicaid programs (37 percent) and health insurance (34 percent). The rest is covered by other state and federal programs such as the Veterans’ Administration, as well as private charity. So, only a dime of the average health care dollar represents payments by patients. The other 90 cents are paid by third parties.[7]

The bulk of private health insurance is employer-provided due to U.S. tax policy wherein employers write off insurance costs as a deduction and avoid payroll taxes on employee compensation that is in the form of benefits. Employees enjoy benefit compensation without income or payroll tax liability. HSA savings enjoy this same tax benefit in a purposeful policy effort to put individual medical expenditures outside of employer-provided insurance on an equal tax footing.

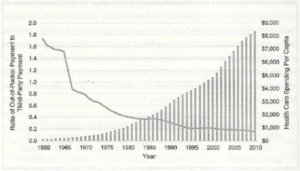

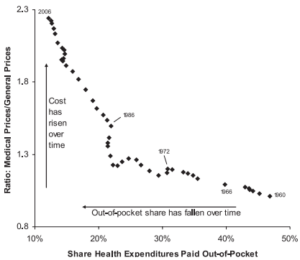

Clearly, due to third-party payments, patients are mostly insulated from what their health care actually costs. Thus, they do not question costly recommended procedures that might not be necessary. Health care providers respond, knowingly or not, by suggesting procedures that are of, at best, marginal value.[8] Excessively high prices are also charged for procedures when providers do not feel as morally constrained as they do in dealing directly with individuals, but see bills as being paid by anonymous monolithic institutions.[9] The consequence is illustrated in Figures 1 and 2 below. Figure 1 shows health care expenditures rising ever more rapidly as the proportion of health care expenditures made out-of-pocket falls. This could be almost entirely due to consuming more health care, but Figure 2 shows that health care has gotten more expensive relative to everything else as the share of spending out-of-pocket has fallen.

Figure 1

Source: Charles Silver and David A. Hyman, Overcharged: Why Americans Pay Too Much for Health Care, (Washington, DC: Cato Institute, 2018), p 288.

Figure 2

Source: Byron Schlomach, Removing the Middleman: What States Can Do to Make Health Care More

Responsive to Patients, Goldwater Institute Policy Report No. 230, January 13, 2009, p 21, https://goldwaterinstitute.org/wp-content/uploads/cms_page_media/2015/2/10/Removing%20the%20Middleman.pdf

Singapore serves as an example of what can happen when incentives in health care are fundamentally impacted by policies that encourage people to save for their own health care expenses and pay for these expenses themselves. This small nation has a relatively healthy population with the share of its GDP devoted to health care a low single-digit percentage, in contrast to the nearly 20 percent of GDP spent on health care in the U.S. The Singapore government’s hand is anything but absent in health care, but everyone except the indigent is expected to cover the bulk of their own health care expenses. Saving for future health care expenses is not optional; it’s required.[10] Consequently, people take care of themselves and, no doubt, act more responsibly in their consumption decisions. Providers truly compete and must act more responsibly as well.[11]

One Way HSA Incentives Are Undermined by Insurance Companies

Traditional health insurance plans pay for the bulk of every health-related expenditure. Patients pay only modest co-payments upfront. So, when a patient shows for an office visit, a cash payment of 20 to 50 dollars might be required, but the bulk of the bill is paid by insurance. Prescription drugs are paid for in much the same way. Co-payments can vary significantly, depending on procedure and setting, but are generally modest compared to total charges billed to insurance. Co-payments count toward a relatively modest deductible, and if they add up to the deductible within a year, co-payments are no longer required the rest of that year and insurance covers virtually 100 percent of many expenses and a larger share of other expenses than it otherwise would have.[12]

High deductible health plans (HDHPs) should work significantly differently from traditional employer-provided health plans. HDHP patients should be considered cash payers who pay the entire charge for services rendered during a year until the relatively high deductible is reached. Basically healthy individuals’ health expenditures would rarely reach the yearly deductible, which would allow savings in an HSA to accumulate. With accumulation beginning relatively early in life, HSA balances would be quite substantial by the time old-age infirmities begin to afflict HSA account holders.

Cash-pay prices in health care are very often lower than prices negotiated by insurance companies.[13] However, even though an individual with an HDHP is often paying the entirety of the bill for a medical service, the insurance-negotiated price is charged instead of the cash price. When an individual with an HDHP presents an insurance card to a provider, that provider is bound by the pricing contracted with insurance and is prohibited from offering a price lower than the contracted price.[14]

Except, perhaps, for circumstances where the insured is traveling or in cases of true emergency, insurance companies do not accept receipts for out-of-network purchases to be counted toward the deductible. In fact, someone with an HDHP could go to an in-network doctor, not use an insurance card, pay the cash price, and insurance would not accept the cash receipt to count toward the deductible, even if the price is lower than the insurance-negotiated price.

For the insured with an HDHP, there is always the possibility that the total dollar amount of services consumed in a year will reach the deductible, even if the HDHP holder only paid lower cash-pay prices. If there is a chance that the deductible will be reached, and insurance companies do not accept cash-pay receipts to be counted toward the deductible, then it makes little financial sense for an HDHP-covered individual to act as a cash-pay customer. A cash-paying individual with an HDHP risks paying much more out-of-pocket by paying cash without presenting an insurance card than if he pays insurance-negotiated prices having presented the insurance card. This pushes those with HDHPs to always present an insurance card and likely get charged more than they would be if they acted as cash payers without insurance.

While it seems like insurance companies would welcome HDHP holders paying lower cash prices, counting these lower sums toward deductibles, since they would appear to save insurance companies money, a few issues arise. First, insurance companies lose a great deal of control. Patients decide what care is appropriate without insurance company input or permission. Though services are obtained at lower prices, insurance companies might think that without their approval an HDHP patient would overuse services and reach their deductible sooner than otherwise, costing the insurance company money. However, this ignores the incentive for patients to economize inherent in HSAs.

Second, perhaps insurance companies are concerned about administrative costs involved in making sure cash-paid services claimed from out-of-network or even in-network to count toward the deductible are legitimate. However, there are phone calls and other administrative time and effort expended for nearly every transaction that involves insurance. Legitimacy of charges are always an issue, whether in-network or not and whether the charge is presented by a provider or in the form of receipt by the insured.

One can only speculate, but it appears that the main reason insurance companies do not accept cash-pay receipts toward HDHP deductibles is that patients might become less dependent on insurance companies. Pressure might even be put on Congress to liberalize the HSA law so that deductibles would be even higher than the current $3,600 per person or $7,200 per family, allowing for lower insurance premiums, greater yearly HSA savings, and even more independence from insurance companies. The real horror from an insurance company perspective would be that peoples’ savings would be sufficient in old age that they would feel secure in buying only the equivalent of the “hospitalization,” truly catastrophic illness, insurance plans of yore.

Solutions

What States Should Do

Most problems with excessive and rising health care prices, particularly the third-party-payer problem, stem from federal policies, especially income tax policy that discriminates against uninsured individual medical expenditures. HSAs are intended to combat this problem, and could be expanded by the federal government to do an even better job of combatting the tax discrimination problem as noted below. But, states are not powerless. They can aid in making good federal policy work even better. With respect to HSAs, states can counter insurance companies’ efforts to undermine their impacts.

Require insurance companies to count self-pay claims for covered services toward a consumer’s deductible, whether the service is performed by an in-network provider or not.

The state can require insurance companies to accept self-pay claims for insured medical services. Someone with an HDHP who pays cash for a medical service without presenting an insurance card should be able to send in the receipt for the purchase, and insurance companies should be required to count that amount toward the deductible. If the cash-pay price is higher than the average charge negotiated with in-network providers, the insurance company should only be required to count that average charge toward the deductible. On the other hand, if the average charge is higher than the claimed cash-pay amount, the average should still count toward the deductible. This would give insurance companies more incentive to drive harder bargains with providers. Insurance companies would still be free to accept or reject claims based on need assessments.

Require insurance companies to inform HDHP participants that cash-pay prices might be lower than insurance-negotiated prices and of procedures to make cash-pay claims.

HDHP participants should not have to figure out for themselves through experimentation that making cash-pay claims is an option. They should be told, and reminded during each open-enrollment period.

Require insurance companies to immediately give any policyholder who asks real-time and meaningful pricing information.

If HSA owners, or anyone else, is to be expected to act as a consumer the same as in any other market, accurate and timely price information must be readily available in medical markets. Timely here means on request and prior to services being rendered and within a specified time period such as 24 hours, the same as in any other market. HDHP participants should be able to call their insurance company and readily obtain the negotiated price for a service and then have the option to call alternative cash-pay providers for comparison. Arguments that this might impair secrecy clauses in the insurer-provider contracts are not sound when HDHP participants: 1) are not direct parties to contracts negotiated and agreed to by their employers, and 2) are not qualified to evaluate the contract provisions in the first place. These secrecy clauses should be made explicitly unenforceable as against public policy.

If service prices are not disclosed by medical service providers prior to services being rendered, prohibit them from civil litigation over unpaid bills in excess of the lowest transparent price(s) for the same service(s) in an area, and prohibit referrals to collections agencies and credit ratings services when prices exceed the same.

There is no such thing as a market when prices are not readily available. Prices are the single most important signal in a market-based economy and are what bring about market efficiencies so that products and services are produced in the most efficient ways possible and those with the highest-valued uses are able to bid for products and services. What’s more, it is immoral, to say the least, for the legal system to be used to favor parties who keep their prices secret until after the service is rendered, and only then reveal prices to the consumer.

What the Federal Government Should Do

Sean Flynn, an economics professor at Scripps College, has suggested that, much as in Singapore, U.S. citizens should be required to have HSAs and make minimum contributions. The interesting thing about this proposal, and the author’s proclivities, is that despite the willingness to use governmental power to regulate and impose certain behavior, Flynn does not suggest effectively socializing medicine with a single-payer model.[15] Instead, he recommends HSAs be heavily liberalized. Similarly, the suggestions below would greatly liberalize HSA policy, but without any type of mandate on individuals to save for health care.

Increase limits on yearly HSA savings, divorced from minimum or maximum health insurance deductibles to at least $10,000 per person or $20,000 for a family.

Allow employers to make tax-free contributions to employee HSAs subject to no limit other than the maximum just mentioned. (Employers could make HSA contributions in lieu of paying insurance premiums.)

Allow HSA owners to pay for health insurance premiums from their HSA without tax penalty. (This would allow for portability from one employer to the next.)

Allow HSA owners to donate HSA balances above a minimum balance (say, $75,000 or a sliding scale that increases with age) to others’ HSAs without tax penalty for either the donor or recipient.

Allow HSAs to be inherited without tax penalty as long as they are maintained as HSAs by heirs.

Conclusion

The bulk of the responsibility for poor policy that results in high and fast-rising medical service prices lies with the federal government. Between its poor stewardship of taxpayer funds under the Medicare and Medicaid programs (the latter including states’ poor stewardship), and restrictive income tax policy that rewards a private third-party payment system in the form of employer-paid health insurance, the federal government is in the best position to right the ship. However, states can and should do their part.

One example of the federal government moving in the right direction is Health Savings Accounts. While the federal government should heavily liberalize this policy direction by removing restrictions on HSAs, the states can take steps to force insurance companies to treat HSA holders with high deductible health plans fairly. Specifically, a policy of allowing HDHP participants with HSAs to claim self-pay medical purchases for deductible purposes, along with informational and price transparency reforms, would increase faith in HSAs as a policy by making the advantages of the policy more obvious. Instead of allowing insurance companies to undermine the policy, such state action would reinforce the policy so that HSAs are used as intended and result in the intended incentives as well.

[1] Stephen Miller, “IRS Announces 2021 Limits for HSAs and High-Deductible Health Plans,” SHRM.org webpage, May 21, 2020, https://www.shrm.org/resourcesandtools/hr-topics/benefits/pages/irs-2021-hsa-contribution-limits.aspx.

[2] “2021 Out-of-Pocket Limits, HDHP Minimum Deductibles, and HSA Contribution Limits,” Medcost.com webpage, July 8, 2020, https://www.medcost.com/employers/resources/news/2021-out-pocket-limits-hdhp-minimum-deductibles-and-hsa-contribution-0.

[3] Ted Godbout, “HSA Assets See Record Growth, Exceed $71 Billion,” National Association of Plan Advisors webpage, April 6, 2020, https://www.napa-net.org/news-info/daily-news/hsa-assets-see-record-growth-exceed-71-billion#:~:text=The%20firm’s%202019%20data%20further,%25%20year%2Dover%2Dyear.

[4] CMS.gov, “Historical,” CMS.gov webpage, accessed February 5, 52021, https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/NationalHealthExpendData/NationalHealthAccountsHistorical#:~:text=U.S.%20health%20care%20spending%20grew,spending%20accounted%20for%2017.7%20percent.

[5] Megan Leonhardt, “Americans Are Spending Down Their Annual HSA Dollars, Using Most of It Just to See Doctors,” CNBC.com, January 23, 2020, https://www.cnbc.com/2020/01/23/americans-are-draining-hsa-and-spending-most-to-see-doctors.html.

[6] Louis Jacobson, “Does Emergency Care Account for Just 2 Percent of All Health Spending?” October 28, 2013, https://www.politifact.com/factchecks/2013/oct/28/nick-gillespie/does-emergency-care-account-just-2-percent-all-hea/.

[7] CMS.gov, “National Health Expenditures 2017 Highlights, CMS pdf document, accessed February 6, 2021,

[8] Arnold Kling, Crisis of Abundance: Rethinking How We Pay for Health Care (Washington, DC: Cato Institute, 2006).

Shannon Brownlee, Overtreated: Why Too Much Medicine Is Making Us Sicker and Poorer (New York, NY: Bloomsbury Publishing, 2010).

[9] Marty Makary, The Price We Pay: What Broke American Health Care–and How to Fix It (New York, NY: Bloomsbury Publishing, 2019).

Charles Silver and David A. Hyman, Overcharged: Why Americans Pay Too Much for Health Care, (Washington, DC: Cato Institute, 2018).

[10] Rowan Callick, “The Singapore Model,” American Enterprise Institute, May 27, 2008, https://www.aei.org/articles/the-singapore-model/.

[11] Sean Masaki Flynn, The Cure That Works: How to Have the World’s Best Healthcare at a Quarter of the Price (Washington, DC: Regnery Publishing, 2019), p 70.

[12] This is a highly simplified explanation of how health insurance works.

[13] Harry Sit, “How I paid cash for health care instead of using my insurance plan — and saved money,” MarketWatch.com, November 22, 2019, https://www.marketwatch.com/story/how-i-paid-cash-for-health-care-instead-of-using-my-insurance-plan-and-saved-money-2019-11-06.

Morgan Boydston and Devin Ramey, “Cash vs. insurance: A little-known option could save you money on medical bills,” KTVB 7 News, February 12, 2019, https://www.ktvb.com/article/news/health/cash-vs-insurance-a-little-known-option-could-save-you-money-on-medical-bills/277-3075953b-6e78-4587-8f0c-ef0da35554b2.

[14] Jay Kempton, President and CEO of The Kempton Group, a 3rd party administrator for self-insured employer health plans, interview by the author, February 9, 2021.

[15] Theodore, McDowell, “Mandatory Health Savings Accounts and the Need for Consumer-Driven Health Care,” Georgetown Journal of Law & Public Policy 16 (Winter 2018), https://www.jw.com/wp-content/uploads/2018/09/MANDATORY-HEALTH-SAVINGS-ACCOUNTS-AND-THE-NEED-FOR-CONSUMER-DRIVEN-HEALT….pdf.

Summary HTML

What States Can Do to Improve Health Savings Account Incentives

Byron Schlomach

Health Savings Accounts (HSAs) are savings accounts wherein:

- Income diverted by an individual to an HSA is not taxed (currently limited to $3,600 for an individual and $7,200 for a family).

- Interest or other earnings that accrue to an HSA are not taxed.

- Withdrawals to pay for medical expenses defined under federal law are not taxed.

- HSA contributions may be made by HSA owners or by employers on behalf of individual employees and/or their families.

- HSA contributions can only be made if an individual is covered by a high deductible health insurance plan.

- Balances may accumulate.

- On retirement, an HSA owner may make withdrawals to spend for non-healthcare purposes without tax penalty, but must pay tax on such withdrawals as income.

By the end of January 2020, HSA assets had grown to almost $72 billion, but this is paltry (less than two percent) when compared to the $3.8 trillion spent on health care in 2019 alone.

Americans regularly spend nearly all of their yearly contributions, possibly because an individual with a high deductible health plan (HDHP) who pays cash to a provider without recourse to insurance will not see that purchase counted toward their deductible.

HSA account holders pay out of their HSAs as insured customers and lose out on substantial cash-pay discounts since they are charged the price agreed to by their insurance company.

Origin of Health Savings Accounts

HSAs were enacted in 2003 partly to help counteract the “third-party-payer” problem in health care.

- There are two major third-party payers in health care – government and employer-paid health insurers.

- Only 10 percent of health care expenditures are paid directly from patients’ pockets.

- Due to third-party payments, patients are mostly insulated from what their health care actually costs and do not question costly recommended procedures that might not be necessary.

- Health care providers respond by suggesting procedures that are of, at best, marginal value.

- Providers also charge excessively high prices for procedures when providers do not feel as morally constrained as they do in dealing directly with individuals, but see bills as being paid by anonymous monolithic institutions.

One Way HSA Incentives Are Undermined by Insurance Companies

High deductible health plans (HDHPs) should work significantly differently from traditional employer-provided health plans.

- Cash-pay health service prices are often lower than those negotiated by insurance companies.

- HDHP patients should be considered cash payers who pay the entire charge for services rendered during a year until the relatively high deductible is reached.

- Except for circumstances where the insured is traveling or in cases of true emergency, insurance companies do not accept cash-pay receipts for out-of-network or in-network purchases to be counted toward the deductible.

- When an individual with an HDHP presents an insurance card to a provider, that provider is bound by the pricing contracted with insurance and is prohibited from offering a price lower than the contracted price.

- If there is a chance that the deductible will be reached, and insurance companies do not accept cash-pay receipts to be counted toward the deductible, then it makes little financial sense for an HDHP-covered individual to act as a cash-pay customer.

- A cash-paying individual with an HDHP risks paying much more out-of-pocket by paying cash without presenting an insurance card than if he pays insurance-negotiated prices having presented the insurance card, pushing those with HDHPs to always present an insurance card and likely get charged more than if they acted as cash payers without insurance.

One can only speculate, but it appears that the main reason insurance companies do not accept cash-pay receipts toward HDHP deductibles is that patients might become less dependent on insurance companies.

Solutions

What States Should Do

- Require insurance companies to count self-pay claims for covered services toward a consumer’s deductible, whether the service is performed by an in-network provider or not.

- Require insurance companies to inform HDHP participants that cash-pay prices might be lower than insurance-negotiated prices and of procedures to make cash-pay claims.

- Require insurance companies and medical service providers to immediately give anyone who asks real-time and meaningful pricing information.

What the Federal Government Should Do

- Increase limits on yearly HSA savings, divorced from minimum or maximum health insurance deductibles, to at least $10,000 per person or $20,000 for a family.

- Allow employers to make tax-free contributions to employee HSAs subject to no limit other than the maximum just mentioned. (Employers could make HSA contributions in lieu of paying insurance premiums.)

- Allow HSA owners to pay for health insurance premiums from their HSA without tax penalty. (This would allow for portability from one employer to the next.)

- Allow HSA owners to donate HSA balances above a minimum balance (say, $75,000 or a sliding scale that increases with age) to others’ HSAs without tax penalty for either the donor or recipient.

- Allow HSAs to be inherited without tax penalty as long as they are maintained as HSAs by heirs.

Conclusion

The bulk of the responsibility for poor policy that results in high and fast-rising medical service prices lies with the federal government. However, states can and should do their part.