Abstracting: Licensure and Regulatory Impacts in Oklahoma

Authors

Mike Davis, with statistical modeling and analysis by Byron Schlomach

Abstract

This paper shows how the licensing of abstracting (title searches made to facilitate real estate transactions) increases costs to home buyers, limits competition and opportunity, and creates unnecessary burdens for home buyers.

Full Text HTML

Abstracting: Licensure and Regulatory Impacts in Oklahoma

Mike Davis

with statistical modeling and analysis by Byron Schlomach

The Oklahoma Abstractors Act [1] has a sunset date of July 1, 2020. The members of the Oklahoma Abstractors Board have staggered, 4 year terms. Abstracting licensure should be allowed to sunset, and no new licensing of the trade should occur. Further, the requirement[2] that a title insurer consult a full abstract created by a licensed abstractor before issuing a title insurance policy should be repealed.

Abstracting

Abstracting is the practice of finding and compiling all relevant legal documents concerning the ownership history of a piece of real property. It is usually done in preparation for the sale of the property; an attorney will then examine the title history to ensure that a seller possesses good title – that is, that no other parties have a legitimate claim of ownership. This is done in an effort to protect the buyer from issues like mechanic’s liens, easements, tax liens, and divided interests in a property. These “clouds” on the title might not be obvious merely from looking at the deed or even from a cursory look at the county records.

While doing a title search is an important part of a real estate transaction, it is no longer the sole protection available to buyers. Title insurance is available to spread the risk of an adverse claim on one title among many titleholders. Because it is backward-looking (covering only the closed world of past events relative to the property, rather than the open world of all possible future events) title insurance tends to be significantly less expensive than forward-looking casualty insurance. And since everything that could impact the title has already happened, title insurance is paid as a one-time fee rather than as a recurring premium.

This backward-looking aspect allows title insurers to more easily determine how much risk they are accepting before they price a policy. Title examiners can trace the roots of a title all the way back to when a government (say the state of Oklahoma or the U.S. Government) owned it. Consequently, there is relatively little risk of a clouded title on a fully researched property. However, these searches can be costly.

There may be times when an insurer determines that it costs more to research every claim back to sovereignty than it does to accept some risk of hidden claims. These older claims tend not to arise, and the Oklahoma Marketable Title Act precludes most (though not all) species of claim if they have gone unrecorded for more than 30 years.[3] So a 30 year title search might well be the most efficient for both the insurer and the insured. The buyer is protected, up to the value of their property at the time the policy was purchased. In all likelihood the insurer could pay off a claimant (someone, other than the insured, claiming an ownership interest) for less than the full value of the land. This efficient allocation of risk saves buyers and insurers money by eliminating most of the risk for a greatly reduced search time. Many states allow this efficient allocation of resources. Oklahoma does not.

Current Law

Oklahoma law requires, de facto, anyone borrowing money to purchase real estate to have a full abstract of title prepared by a licensed abstractor, and examined by a licensed attorney. The law’s mandate falls exclusively on title insurers, making it illegal to issue a title insurance policy unless a licensed attorney examines the title history prepared by a licensed abstractor.[4] Since Freddie Mac and Fannie Mae require title insurance before they will buy a mortgage, banks are unwilling to loan money without title insurance.[5][6] So both an abstractor and an attorney are necessary for almost every real estate transaction in the state. Even in self-financed purchases, title insurance may be needed or desired.

Oklahoma requires abstractors (and lawyers[7]) to have a license to practice their profession. Title abstracting is defined by statute as “a person working for a holder of a certificate of authority to search and remove from county offices county records, summarize or compile copies of such records, and issue the abstract of title.”[8] The Oklahoma Abstractors Board oversees the licensing of individual abstractors as well abstracting companies. The board also approves the rates abstractors charge, though they do not set the rates as such.

A controlling majority of the board – six of the nine members – must be licensed abstractors with at least five years of experience in the industry, each representing one of six geographic districts. The remaining three members must be one attorney, one real estate agent, and one officer of a bank, each with 5 or more years of experience. The board has the ability to approve or disapprove members of the Abstracting industry, approve or disapprove abstracting companies within a given county (they can approve a company for one county but disapprove it for another) and the power to approve or disapprove rate sheets for each company. Thus, the industry is self-regulated, but with the might of state government behind it.

The governor has the power to remove board members, but only in very limited circumstances. Should a member or a majority of the board go rogue, the governor would have little recourse on his own. The law is worded such that, except in narrow and carefully worded circumstances, it would take a judicial finding (guilty of a crime, mental incompetence, etc.) or the aid of a majority of the board for the governor to remedy the situation.[9]

Three separate phases of the industry are regulated by statute: 1) A permit is required to begin building an abstract plant; 2) a Certificate of Authority is required to operate the abstracting business;[10] and 3) individual abstractors must acquire a license from the board.[11] In addition, abstractors must carry Errors and Omissions Insurance or a bond, with coverage ranging from $15,000 for counties with the smallest populations, to $100,000 for the most populous counties.[12]

An abstract plant is a copy of, and system of cataloging, every legal document relating to every piece of property in a given county. Once approved to build an abstract plant, a company has one year to complete the process, or apply for a permit renewal.[13] When the plant is completed to the satisfaction of the Abstractors Board, The Certificate of Authority allows an abstracting company to hire licensed abstractors and gives them authorization to issue abstracts of title.

Acquiring an abstracting license entails passing a test as well as approval by the abstracting board. Applicants must be 18 years old, of good moral character, and free of convictions for felonies and crimes of “moral turpitude.” Anyone possessing these qualifications and passing the test “shall be issued” a license, with the board given discretion to determine good moral character.

Burden

Overall, the practice of occupational licensing costs the country as many as 1.9 million jobs and over $180 billion in GDP due to economic impacts like deadweight loss and other market inefficiencies.[14] Abstracting restrictions in Oklahoma certainly contribute to the problem.

The national average cost[15] of title insurance plus title examination or abstracting for a $250,000 home is $1,421. In Oklahoma these services are likely to run closer to $1,708 when adjusted for the cost of living. In fact, the 12 states that require title insurers to use an abstracting plant average $1,545 while those that do not, average $1,380. This 10 percent premium understates the issue in Oklahoma, where the 25 percent premium over the national average is likely due to the necessity of having title plants that date back as far as the county clerk has records. Some abstracting plant states require only 25, 45, or 50 years, and come in closer to the national average.[16] Other states requiring a full title plant containing copies of all county records are similarly above the national average.[17] Texas is an exception: in spite of requiring a plant to start not later than January 1, 1979, the state has an estimated cost of $1,978.[18] Wyoming is an exception in the opposite direction, with an estimated cost of only $1,066 despite requiring a full title plant.[19]

The costs do not fall on consumers alone; would-be entrepreneurs are also harmed. Anyone wishing to become an abstractor in Oklahoma must pay $150 per year in fees, and pass an exam. But an abstracting license does not entitle an individual to work as a sole practitioner. Licensed abstractors may only conduct abstracting business as employees of a company with a Certificate of Authority. And anyone working for such a company in the role of abstractor must be licensed. The burden of creating a title plant, in order to open a new abstracting company, is so expensive and time consuming that new firms decline to enter even those Oklahoma counties that have only one abstractor. This stifles entrepreneurship and precludes innovation in the abstracting industry. From January 2016 to May 2019 (the latest data available at the time of publication), only 5 new Certificates of Authority were granted by the Oklahoma Board of Abstractors.[20]

According to information published by the American Land Title Association (ALTA), Oklahoma’s title insurance industry employs 2,203 title professionals with only 160 title company offices.[21] This includes abstractors as well as title insurance agents and underwriters.[22] By contrast Alabama, with almost 1 million more people than Oklahoma, employs only 1,299 title professionals spread over 120 more (280 total) title offices.[23]

This comparison to Alabama implies that Oklahoma’s laws create more work for title professionals while reducing competition among title companies. A survey of Oklahoma’s closest neighbors in population and geography reveals this is a consistent pattern, not an anomaly. Connecticut, with slightly fewer people than Oklahoma, is a reasonable comparison. It employs only 767 professionals, working across 400 title companies, while issuing 33,420 mortgages. Oregon is an outlier like Oklahoma, having 2,081 professionals in 150 offices for a state with a population about the same size as Oklahoma’s.[24]

While the number of professionals and offices in Oregon roughly equal those of Oklahoma, Oregonians took out 55,500 mortgages as compared to Oklahomans’ 38,120. Oregon’s title laws are fairly restrictive, requiring title insurers to maintain an abstracting plant. However, the plant only need go back 50 years,[25] as opposed to Oklahoma, where a title plant must date all the way to sovereignty.[26]

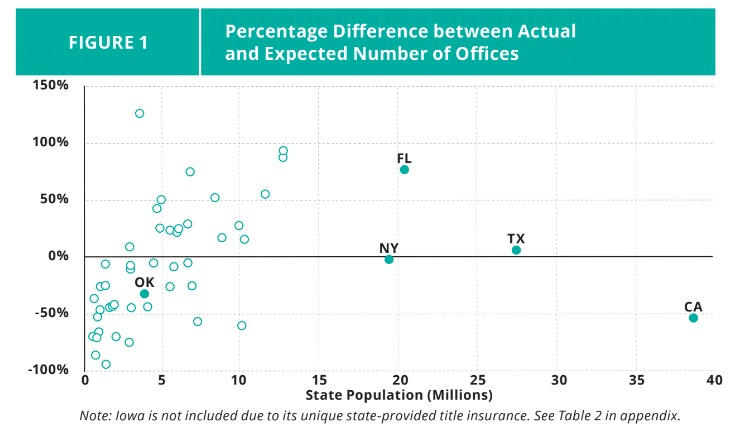

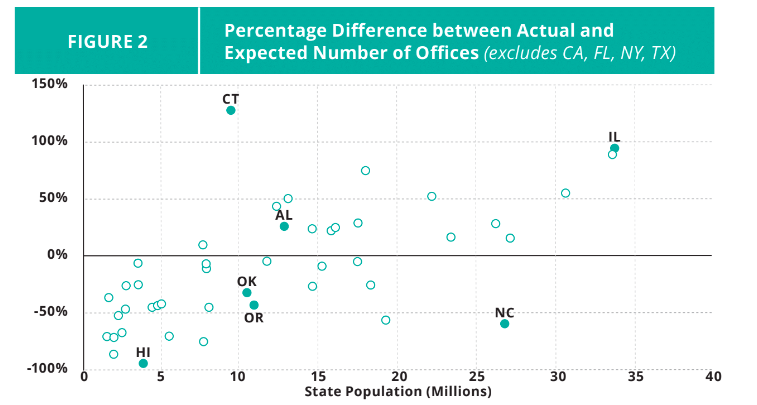

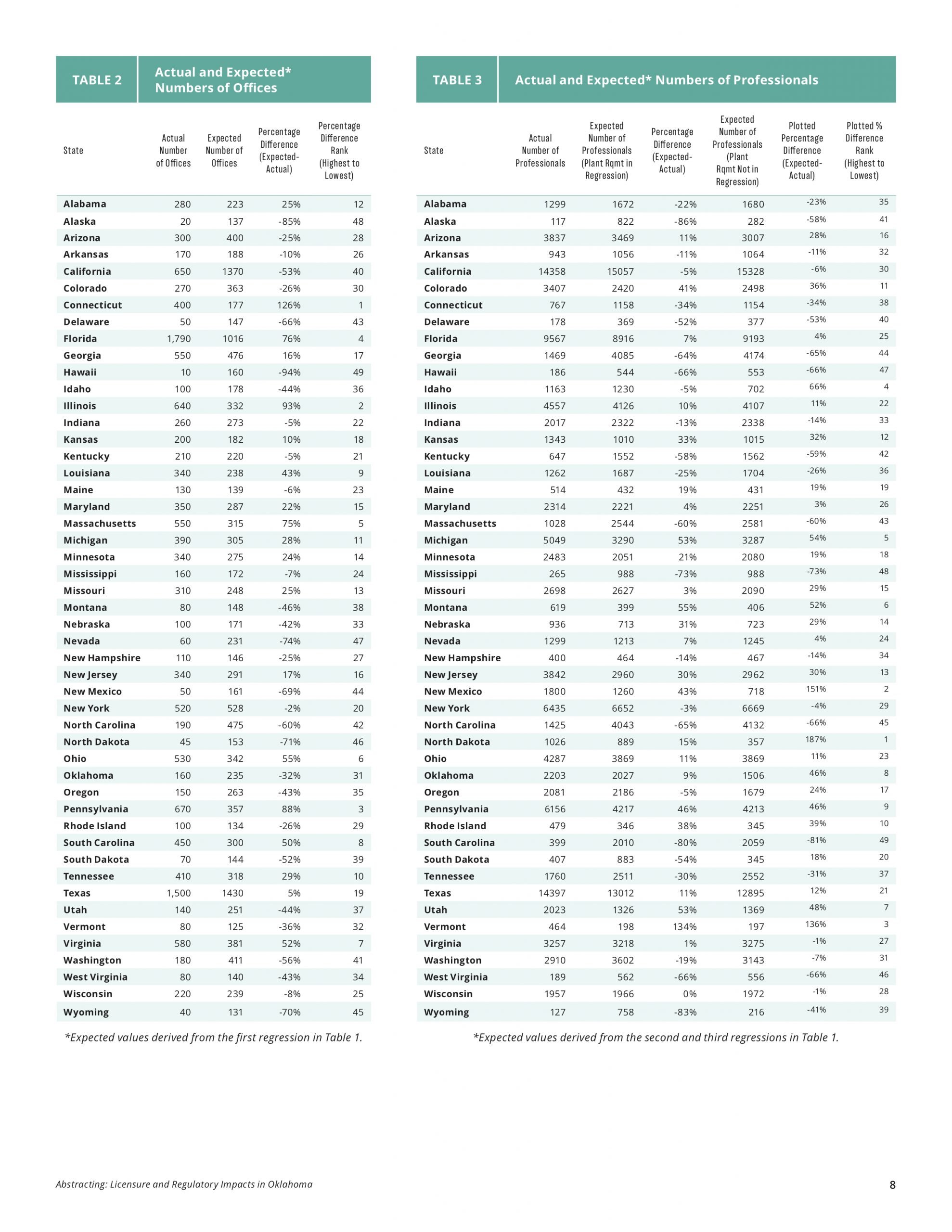

A statistical analysis of the ALTA data for all fifty states, controlling for land area, total population, and gross population growth, reveals that Oklahoma has more people employed in the title industry, working for fewer firms, than most other states in the country.[27] This is exactly the pattern one would expect in a state that throws up high barriers to entry (like requiring a title plant, with an index created from scratch, dating back to sovereignty) for new firms, while also creating a great deal of work for individual title searches (by requiring they go back to sovereignty, rather than a set number of years). These anticompetitive policies can be shown in two sets of charts, using data compiled from the American Land Title Association and derived from the statistical analysis described in the appendix.[28]

Figures 1 and 2 show the percentage difference in the actual number of title searching offices (an imperfect proxy for the number of firms) and the number that would be statistically expected in a state taking population and population growth into account (See Appendix). The only difference between Figures 1 and 2 is that Figure 2 excludes the largest states in population for illustration purposes. Note that Oklahoma has 32 percent fewer offices than would be expected according to the statistical analysis in the appendix. Alabama, and especially Connecticut, on the other hand, have far more offices than would be expected.

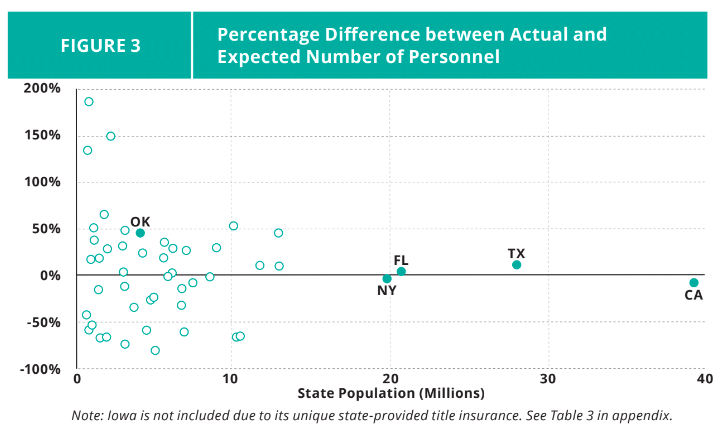

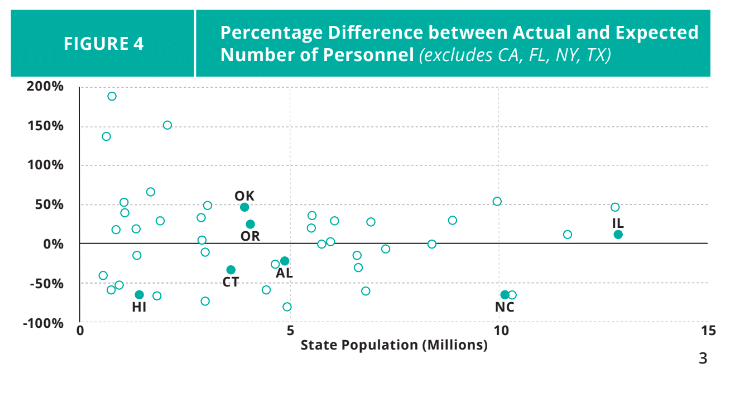

Figure 3: Percentage Difference between Actual and Expected Number of Personnel

Figures 3 and 4 show the percentage difference in the actual number of title searching professionals and the number that would be statistically expected in a state taking population and population growth into account (See Appendix). Again, Figure 4 only excludes the largest states in population for illustration purposes. Note that Oklahoma has 46 percent more professionals than would be expected according to the statistical analysis in the appendix. Only seven states have comparatively more. Alabama, and especially Connecticut, on the other hand, have far fewer professionals than would be expected, despite having a relatively high number of offices.

The appendix describes a statistical analysis that takes into account some states’ requirement that abstractors establish plants, in addition to population and population growth. It was found that plant establishment requirements do have a significant impact on the number of professionals. On average, a plant requirement adds 545 more professionals to a state’s abstracting workforce. The plant requirement impact on the number of professionals is so large that statistically taking it into account makes Oklahoma not appear to be outside the norm in number of professionals when, in fact, Figures 3 and 4 show that it clearly is, with only twelve states requiring abstract plants. The fact that accounting for whether or not a state has a plant requirement takes Oklahoma from significant outlier to just another dot among the cluster serves to highlight just how anticompetitive the requirement is.

Oklahoma is not much of an outlier in terms of number of offices. Eighteen states have fewer offices than expected to a greater extent than the Sooner State. This is likely because Oklahoma law forbids an abstracting company to serve a county in which it does not have an office. Without that requirement, there would likely be far fewer offices. On the other hand, only seven states have comparatively more professionals than would be expected. While Oklahoma cannot be described as unique, it is certainly one among a small number of states that can be described as outliers in terms of simultaneously being on the low end of the number of offices and on the high end of number of professionals.

Population and population changes accounted for most of the variation in both offices and personnel across states. However, Oklahoma is among the least consumer-friendly states. This is shown by the high number of workers, reflecting the high volume of work required by law (a large portion of which is likely unproductive, costing more than the risk it eliminates) and also by the low number of offices despite the mandate of an office for every county, implying that there are relatively few competitors in the field – which is universally bad for consumers.

The facts, illustrated and explained, highlight that Oklahoma creates a lot of busywork for Abstractors to do, and that the state puts up high barriers to entry into the field. This is exactly the situation on the ground. Abstractors have to search the history of a parcel all the way back to when it was owned by a government entity. And the requirement that each firm own an abstracting plant, which contains an independently indexed chart (that is, an abstractor may not copy the index from the county) of every record in the county recorder’s office means that only a few firms will find the time and expense worth the eventual payoff. It can take years to build a plant, as evidenced by the Abstractors Board’s liberal policy when it comes to renewing permits to build a plant (which are good for one year).[29]

1889 undertook a review of whether each state required abstractor licensing, whether it mandated the use of an abstracting plant, and whether it had a Marketable Record Title Act, legislation which purports to facilitate easier real estate transactions by limiting most kinds of clouded title to a given number of years. Two patterns emerged from this analysis: First, states with licensed abstractors tended to be less competitive than states that did not require abstracting licenses. Second, requiring a title plant, whether via a licensed abstractor, or as a condition to licensing the title insurer, had arguably a greater anticompetitive impact.

Surprisingly, the existence or not of a Marketable Record Title Act had almost no impact on a state’s competitive landscape. States with and without Marketable Record Title Acts can be found on both extremes of the competitiveness chart, and spread throughout the middle as well.

There are some inherent weaknesses in this data set which must be acknowledged. First, the number of offices is an imprecise proxy for the number of firms. It certainly overestimates the number of firms in almost all cases. It is quite likely that in every state at least one firm will own more than one office. This is especially true in states like Oklahoma, which require the firm to be located in the county for which it is providing abstracting services.[30]

Second, in states where attorneys are permitted to provide abstracting services, it is quite likely that these attorneys provide many other services while doing title work part time. Therefore, the number of workers engaged in titling work may imply comparatively more man hours than are actually expended. Nevertheless, in a state like Oklahoma where workers are specialized, one would expect them to work more hours on titling than attorneys who might also be drafting wills and filing civil suits to fill their work week. Both of these potential errors cut against Oklahoma. To the extent they are skewed, they skew to understate just how bad the problem is in Oklahoma.

The burden for home buyers is hard to calculate in dollars, because each state requires different protections, and many of them allow a title company to bundle and bill for all the services needed to issue the policy, including the underwriting and the title search. This makes an apples-to-apples comparison across states impracticable.[31]

As of June 2019, an update to an existing abstract when the current owner has owned the property for at least 6 months costs $550 at every abstractor licensed to do business in Oklahoma County.[32] While the board has stated[33] that they do not set rates, the fact that they legally approve rates facilitates price signaling, and pushes firms toward uniform pricing.

Diffuse Costs, Concentrated Benefits

Occupational licensing persists in spite of the well-documented downsides for one reason: the system produces great gains for a few, who have an incentive to preserve it, while the people who stand to lose do so only a little at a time with each new licensing scheme the legislature passes. When a new licensing regime is proposed (almost always by members of the industry to be regulated), the average consumer is likely unaware. If they do happen to catch wind of the bill, they probably think little of it. The cost of any one licensing scheme does not hit the wallet of any individual consumer very hard. It’s only the cumulative effect that is so damaging to consumers and the wider economy. On the other hand, members of licensed and regulated industries tend to fair well, especially those in an industry entrenched in industries as indispensable as land sales.

Evaluating Whether to Continue Abstractor Licensing and Abstract Requirement

The 1889 Institute argues in its Policy Maker’s Guide to Evaluating Proposed and Existing Professional Licensing Laws,[34] that there are two reasons to license an occupation: 1) an occupation’s practices present a real and probable risk of harm to the general public or patrons if practitioners fail to act properly; AND 2) civil-law or market failure makes it difficult for patrons to obtain information, educate themselves, and judge whether an occupation’s practitioners are competent. A third important consideration is whether licensure materially reduces these risks. Consumers bear, indirectly, the costs not only of compliance with the regulatory regime, as these costs are passed on through higher prices, but also the costs of reduced competition. Fewer firms engaged in a practice leads to less innovation and higher prices. These costs should only be imposed if there is both a real danger, and if imposing the costs will really alleviate it.

Do abstractors inherently present a real and highly probable risk of significant harm to patrons if practitioners fail to act properly?

In a word: no. In fact, there would be no inherent risk to eliminating the practice of abstracting from the process of buying real property. Abstractors do provide a valuable service: collecting the documented history of a piece of land, so that an attorney can make sure the seller truly holds clear title. But there is a problem with the way the law is currently written. As it stands now, consumers of abstracting services are forbidden from choosing the level of protection they feel is appropriate. Insurers are not able to choose the level of detail or the length of history they feel is appropriate for a given property, or simply handle the whole process internally.

Title insurers are highly focused professionals. They too must obtain a license to work in Oklahoma.[35] So these professionals should have the ability to decide how much risk they are willing to underwrite. That’s what insurers do. Abstracting is enshrined in state law because insurers were on the verge of disrupting their business model by offering buyers another way to protect themselves. In most states, insurance has made a fully comprehensive title abstract an unnecessary cost, while title checks – a much shorter and less costly process – have become the new default. In these other states, no one is forbidden from getting a full abstract if they need extra peace of mind or enjoy learning the history of their property. Otherwise, insurers accept the risks of insufficient research leading to a clouded title, and consumers are protected by the insurance. After all, the insurer has to compensate both the bank and the homeowner if title ultimately transfers to someone else. There are minimum capital and surplus requirements to guarantee that insurers have enough assets to cover their risks. [36]

Regardless of the level of risk insurers are willing to accept, and how much research they choose to require, they are on the hook if it turns out their bets were bad. Consumers have nothing to fear from the elimination of the entirety of Title 1 of the Oklahoma Statutes, the law that regulates abstractors. Consumers would gain even more benefit from a repeal of 36 O.S. § 5001(C) and any accompanying regulations[37] which requires the use or ownership of title plants before insurance policies may be issued. Regardless of whether abstractors are involved at all, consumers who purchase title insurance will be covered if there is a cloud over their title. Abstractors may reduce the risk of clouded title. If insurers want to accept the risks, however, they should be allowed to do so.

In a free market, insurers can be trusted to make fiscally efficient choices – they will find the optimal balance of looking into a title history and risk. If they make too many bad bets, they will invest in more research. If they find they are spending more on research than they are saving in reducing bad titles, they will reduce the depth of their research. If they find that the best practice is to continue using abstractors, they will. If they want to hire someone else to investigate title histories, they should be allowed to do so. They bear the risk entirely. Consumers win when private companies can decide questions like this for themselves. Competition will drive title insurers to provide the best service at the best price. Right now, insurers are barred from finding these efficiencies. They are required by law to do more than optimal research. Imagine if a restaurant were required to sell eight pounds of rice with every meal they serve. How much food would be wasted? The same scenario is playing out in title insurance and abstracting, but the waste is time and money, instead of rice and money.

Is there a failure of civil law or free markets that makes it difficult for patrons to obtain information, educate themselves, and judge whether an occupation’s practitioners are competent?

No. Again, the consumers of title abstracts are title insurance professionals. They work in this world every day. They know where the risks are. It might be better if they had more direct control over the process of title checks. They might feel they are buying more information than they need since the odds of something from the last 30 years clouding a title are much greater than the odds of something from the 70 years before that. It might be cheaper for insurers to simply pay their insured in the rare cases where an older document changes the ownership, than to investigate every title all the way back to statehood. Unfortunately, this business judgment, which has no impact on consumers, other than the prices they pay for title insurance and abstracting combined, was taken away by overeager legislators decades ago.

While the practice of insurers seeking the advice of competent attorneys and abstractors may well be the best and most efficient course of business, it must be left up to these businesses, not the legislature or an unelected licensing board, to decide.

Policy Recommendations

Nothing in this paper should be taken to denigrate the role of abstractors or title insurers in ensuring the smooth functioning of the real estate market. Quite the opposite: ensuring the continued success of the real estate market by helping property owners make sure their title is clear is so important that we cannot afford to let state government manipulate the market for these vital services. Nor should claims that there exist more efficient title insurance solutions be taken to mean that the title insurance industry is without fault. It is a similarly over-regulated field, and critiques of the industry should be given due consideration.[38] Property buyers should be allowed to choose the type and scope of protections for their title. Insurers should be allowed to accept transfer of risk they deem appropriate based on sound actuarial methods. Abstractors should be able to rely on county records, some of which are already computerized and searchable.[39] Anyone who understands how to look for clouds on a title should be allowed to work as an abstractor. To these ends, the following policies are recommended.

Eliminate Title Plant Requirements

This single recommendation would greatly reduce the harm of both abstractor licensing and the abstracting requirement for title insurance. Eliminating this barrier to entry alone, by letting abstractors rely on county records, would allow a truly competitive market to emerge.

Eliminate Abstracting as a Legally Necessary Component of Title Insurance

A more efficient allocation of resources will occur when title insurers choose the amount of risk they are willing to bear insuring a title (i.e., how far back they want to look into a title history) while fully guaranteeing insureds that clouded title losses will be covered. Insurers will determine the optimal amount of research to put into each property to reduce the total cost of losses plus research time. Consumers will still be quite free to request a deeper look into the history of the property, for a price.

Eliminate Abstractor Licensure

There are neither inherent risks nor market failures that make abstracting an industry from which consumers need such heavy-handed protection, nor is licensure the kind of remedy for the risks inherent in abstracting. Anyone should be free to practice the trade, provided they are bonded or carry an Errors and Omissions policy.

Private Certification

Abstractors could be privately certified as outlined by the 21st Century Consumer Protection & Private Certification Act, available as part of “A Win-Win for Consumers and Professionals Alike: An Alternative to Occupational Licensing,” available at https://1889institute.org/licensing.html. It would allow professionals who form private certifying associations to enforce private credentials through criminal fraud enforcement instead of costly civil actions if a certifying organization follows certain practices, including certain transparency and disclaimer requirements.

It must be noted that the use of private certification would not fully relieve the citizens of Oklahoma of the high costs of mandatory abstracting. The laws enshrining it in the real estate transaction process will always create monopoly pricing schemes. Oklahomans would benefit from a free market for real estate services, just as they benefit from the free market for real estate property.

Appendix

Except for Iowa, where title insurance is purchased from the state, and the state has a title insurance monopoly by law, the most recent data available for each state were collected regarding:

- the number of abstracting professionals

- the number of abstracting offices

- the number of mortgages

- total population in 2016

- the change in population between 2010 and 2016

- and total land area

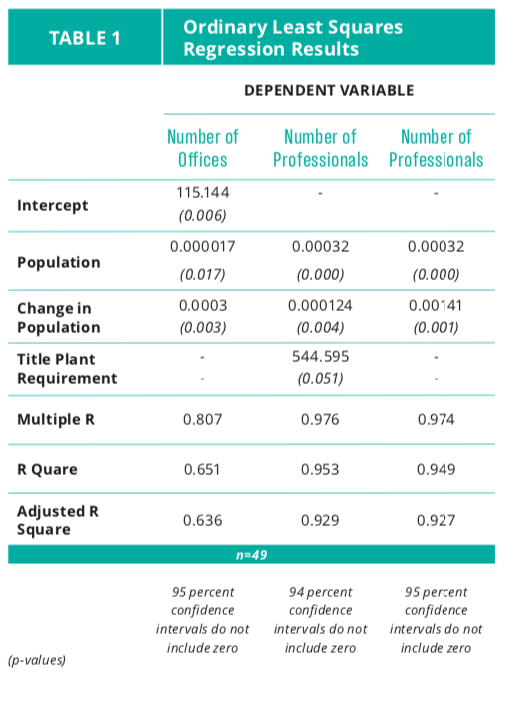

The number of abstracting professionals and the number of abstracting offices were each separately interpreted as dependent variables with the other four variables interpreted as possible explanatory variables. Using linear regression, it was first found that the number of mortgages is highly correlated to total population and population change. Therefore, regressions were run using total population, gross population change, and total land area as explanatory variables.

Total land area showed no statistical significance, probably because so many of the states are large in area but very small in population while others with small areas are large in population. This historical artifact of the development of the United States renders land area useless as an explanatory variable in this analysis.

The results from running linear regressions separately with the number offices and the number of professionals as separate dependent variables and population, population growth, and the requirement to establish a plant (this last, a dummy variable with 1 for the requirement and 0 for no such requirement) as explanatory variables yielded some strong results. These are shown in the following table.

The intercept in the regression with number of professionals as the dependent variable is not statistically significant, and was dropped. All three regressions have strong R values with most of the variation across states explained by population and population growth. These regression coefficients were used to calculate the expected values in Tables 2 and 3 below, which were used to construct Figures 1 through 4 above.

The results of two separate regressions with number of professionals as the dependent variable are reported for two reasons. First, some might argue that the title plant requirement (left out of the second regression) is not a significant explanatory variable given its p-value. However, 94-percent confidence intervals do not include zero for any of the explanatory variables in that regression, including the title plant requirement. The plant requirement clearly does have an impact on the number of abstracting professionals in a state. Second, the last regression is the one used to calculate the expected values in Table 3, and used to construct Figures 3 and 4 to illustrate the outlier nature of Oklahoma, given the relative rarity of title plant requirements.

________________________

-

- 1 O.S. § 1-20 (2018), et seq. As of publishing, the state website still reflects the prior version of this law, but Governor Stitt signed HB 1434 into law on April 15, 2019. http://www.oklegislature.gov/osstatuestitle.html This paper reflects the new sunset date of 2020. ↑

- 36 O.S. § 36-5001(C) (2018). https://law.justia.com/codes/oklahoma/2018/title-36/section-36-5001/ ↑

- 16 O.S. § 16-71 (2018), et seq. https://law.justia.com/codes/oklahoma/2018/title-16/section-16-71/ ↑

- 36 O.S. § 36-5001(C) (2018). ↑

- Freddie Mac Single Family Guide 3401.6 ↑

- Fannie Mae Selling Guide B7-2-01: Provision of Title Insurance ↑

- See Benjamin M. Lepak, The Oklahoma Supreme Court’s Unchecked Abuse of Power in Attorney Regulation, 1889 Institute Policy Report, February 2019, https://1889institute.org/licensing. ↑

- 1 O.S. § 1-21(3) (2018). https://law.justia.com/codes/oklahoma/2018/title-1/section-1-21/ ↑

- 1 O.S. § 1-22(H) (2018). https://law.justia.com/codes/oklahoma/2018/title-1/section-1-22/ ↑

- 1 O.S. § 1-30 (2018). https://law.justia.com/codes/oklahoma/2018/title-1/section-1-30/ ↑

- 1 O.S. § 1-38 (2018). https://law.justia.com/codes/oklahoma/2018/title-1/section-1-38/ ↑

- 1 O.S. § 1-27 (2018). https://law.justia.com/codes/oklahoma/2018/title-1/section-1-27/ ↑

- 1 O.S. § 1-34 (2018). https://law.justia.com/codes/oklahoma/2018/title-1/section-1-34/ ↑

- Morris M. Kleiner, Ph.D. and Evgeny S. Vorotnikov, Ph.D, At What Cost?, Institute for Justice, November 2018, https://ij.org/wp-content/uploads/2018/11/Licensure_Report_WEB.pdf ↑

- 1889 used the closing costs estimation tool at https://facc.firstam.com/ to estimate the insurance premiums for each state, using the most populous county in each state, and a hypothetical residential property purchased for $250,000 with 0 percent down. Where the title fee calculator estimated abstracting fees this estimate was used. In states where title examination is included in the quoted rate, no other fees were added. For the remaining states a good faith effort was made to find representative title exam or abstracting fees and these fees were added to the insurance premium. Finally, each value was adjusted to the national average cost of living, so that, as near as possible, each value represents equal buying power. The figures used for this adjustment are available at https://www.missourieconomy.org/indicators/cost_of_living/.This number was chosen because in theory one would expect a more thorough search to result in fewer payouts, and therefore lower insurance premiums. Thus one would hope this total number would be similar across states regardless of how the total was divided between premiums and research. One would, however, be disappointed in the real world results. ↑

- Alaska Statutes Title 21.66.200. Estimated cost: $1,085. https://law.justia.com/codes/alaska/2017/title-21/chapter-66/section-21.66.200/.Revised Statute of Missouri 381.031.22. Estimated Cost: $1,491. https://law.justia.com/codes/missouri/2014/title-xxiv/chapter-381/section-381.031/. See NOTE at https://insurance.mo.gov/laws/definitions.php as to the current status of this law (still in effect as of June 11, 2019).Oregon Revised Statute 731.438. Estimated Cost: $986. https://law.justia.com/codes/oregon/2017/volume-16/chapter-731/section-731.438/. ↑

- Arizona Revised Statutes 20-1567-B. Estimated cost: $2,129. https://law.justia.com/codes/arizona/2018/title-20/section-20-1567/.Idaho Code 41-2702. Estimated Cost: $1,683. https://law.justia.com/codes/idaho/2017/title-41/chapter-27/section-41-2702/.Revised Code of Washington 48.29.160. Estimated Cost: $1,761. https://law.justia.com/codes/washington/2018/title-48/chapter-48.29/section-48.29.160/.South Dakota Code 36-13-10. Estimated Cost $1,261. https://law.justia.com/codes/south-dakota/2018/title-36/chapter-13/section-36-13-10/.New Mexico Statutes – Section 59A-12-13. Estimated cost: $1641. https://law.justia.com/codes/new-mexico/2017/chapter-59a/article-12/.

North Dakota Century Code Title 43. Occupations and Professions § 43-01-09. Estimated cost: $1910. https://law.justia.com/codes/north-dakota/2017/title-43/chapter-43-01/. ↑

- Texas Statutes Insurance Code Title 11 §2501.004. https://law.justia.com/codes/texas/2017/insurance-code/title-11/subtitle-a/chapter-2501/ ↑

- WY Stat § 33-2-101. https://law.justia.com/codes/wyoming/2017/title-33/chapter-2/section-33-2-101/ ↑

- Minutes of Oklahoma Abstractors Board Meetings available at; https://www.ok.gov/abstractor/Agendas_and_Minutes/The 2016 minutes have been removed from the site, but according to 1889’s review, no new CoA’s were issued in 2016. One was issued in 2017, three were issued in 2018, and one has been issued so far in 2019. ↑

- American Land Title Association, May 2018, This data was originally found on the “Advocacy” section of ALTA’s website, last accessed in December of 2018. ALTA has since taken these documents down, however Google has archived HTML versions which can be viewed by doing a Google search for the phrase “the title insurance industry employs”, clicking “repeat the search with the omitted results included”, and selecting “Cached” from the green arrow next to the link for each state.A direct link to the archived version of the Oklahoma data is available at: https://webcache.googleusercontent.com/search?q=cache:7a8cM8UFoX0J:https://www.alta.org/media/PDF/advocacy/state-data/Oklahoma.pdf+&cd=1&hl=en&ct=clnk&gl=us ↑

- https://www.alta.org/about/ ↑

- Ibid. ↑

- Ibid. ↑

- Oregon Revised Statute 731.438. ↑

- 1 O.S. 1-21 (2018). https://law.justia.com/codes/oklahoma/2018/title-1/section-1-21/ ↑

- See Appendix. ↑

- See Appendix. ↑

- 1 O.S. § 1-34 (2018). https://law.justia.com/codes/oklahoma/2018/title-1/section-1-34/ ↑

- 1 O.S. § 1-21-6 (2018); 1 O.S. § 1-27 (2018). https://law.justia.com/codes/oklahoma/2018/title-1/section-1-27/ ↑

- The government accountability office came to the same conclusion. Actions Needed to Improve Oversight of the Title Industry and Better Protect Consumers, Report to the Ranking Member, Committee on Financial Services, House of Representatives, United States Government Accountability Office, Page 19. See: https://www.gao.gov/new.items/d07401.pdf ↑

- https://www.ok.gov/abstractor/Abstractor_Directory_&_Rates/index.html ↑

- Oklahoma Abstractors Board Minutes November 2017. https://www.ok.gov/abstractor/documents/Minutes%20November%2021,%202017.pdf ↑

- Available at https://1889institute.org/licensing.html. ↑

- 36 O.S. § 36-1101 (2018). https://law.justia.com/codes/oklahoma/2016/title-36/section-36-1101/ 36 O.S § 36-1435.4(2018). https://law.justia.com/codes/oklahoma/2018/title-36/section-36-1435.4/ ↑

- 36 O.S. § 36-610 (2018). http://www.oscn.net/applications/oscn/DeliverDocument.asp?CiteID=86281 ↑

- Including but not limited to OAC 365:20-3-2, 365:20-3-3(a)(1), 365:20-3-3(a)(4), and 365:20-3-3(b). https://www.ok.gov/oid/documents/091214_Chapter%2020%20Subchapter%203.pdf ↑

- Scott Woolley, “Inside America’s Richest Insurance Racket,” Forbes, October 28, 2006, https://www.forbes.com/forbes/2006/1113/148.html#640e61215266. ↑

- See e.g. Oklahoma County. https://okcc.online/ ↑