Multilateral Disarmament: A State Compact to End Corporate Welfare

Authors

Byrson Schlomach, Stephen Slivinski, James Hohman

Abstract

This paper (jointly published by the Mackinac Center for Public Policy and the 1889 Institute) comprehensively discusses various forms of corporate welfare, corrects the New York Times‘ ranking of states based on corporate welfare granted, and proposes a comprehensive solution for ending corporate welfare across the states.

Full Text HTML

The Mackinac Center for Public Policy is a nonpartisan research and educational institute dedicated to improving the quality

of life for all Michigan residents by promoting sound solutions to state and local policy questions. The Mackinac Center assists policymakers, scholars, businesspeople, the media and the public by providing objective analysis of Michigan issues. The goal

of all Center reports, commentaries and educational programs is to equip Michigan residents and other decision makers to better evaluate policy options. The Mackinac Center for Public Policy is broadening the debate on issues that have for many years

been dominated by the belief that government intervention should be the standard solution. Center publications and programs,

in contrast, offer an integrated and comprehensive approach that considers:

All Institutions. The Center examines the important role of voluntary associations,

communities, businesses and families, as well as government.

All People. Mackinac Center research recognizes the diversity of Michigan residents and treats

them as individuals with unique backgrounds, circumstances and goals.

All Disciplines. Center research incorporates the best understanding of economics, science, law,

psychology, history and morality, moving beyond mechanical cost‑benefit analysis.

All Times. Center research evaluates long-term consequences, not simply short-term impact.

Committed to its independence, the Mackinac Center for Public Policy neither seeks nor accepts any government funding. The Center enjoys the support of foundations, individuals and businesses that share a concern for Michigan’s future and recognize the important role of sound ideas. The Center is a nonprofit, tax-exempt organization under Section 501(c)(3) of the Internal Revenue Code. For more information on programs and publications of the Mackinac Center for Public Policy, please contact:

Mackinac Center for Public Policy 140 West Main Street P.O. Box 568 Midland, Michigan 48640

989-631-0900 Fax: 989-631-0964 Mackinac.org mcpp@mackinac.org

© 2019 by the Mackinac Center for Public Policy, Midland, Michigan

ISBN: 978-1-942502-34-0 | S2019-04 | Mackinac.org/s2019-04

140 West Main Street P.O. Box 568 Midland, Michigan 48640

989-631-0900 Fax 989-631-0964 Mackinac.org mcpp@mackinac.org

The Mackinac Center for Public Policy and 1889 Institute

Multilateral Disarmament: A State Compact to End Corporate Welfare

By Byron Schlomach, Stephen Slivinski and James Hohman

©2019 by the Mackinac Center for Public Policy and 1889 Institute

Midland, Michigan

Guarantee of Quality Scholarship

The Mackinac Center for Public Policy is committed to delivering the highest quality and most reliable research on Michigan issues. The Center guarantees that all original factual data are true and correct and that information attributed to other sources is accurately represented.

The Center encourages rigorous critique of its research. If the accuracy of any material fact or reference to an independent source is questioned and brought to the Center’s attention with supporting evidence, the Center will respond in writing. If an error exists, it will be noted in a correction that will accompany all subsequent distribution of the publication. This constitutes the complete and final remedy under this guarantee.

Contents

The Most Common Types of Corporate Welfare 4

Deal-closing funds and grants 5

What is Not Corporate Welfare? 9

What’s So Bad About Corporate Welfare? 10

Ranking the States: Improving the New York Times Corporate Welfare Ranking 13

An Alternative to Subsidies: Healthy State Competition 16

Reining in Corporate Welfare 18

Achieving Healthier State Competition with a “Cease-Fire” Agreement 18

Appendix: Corporate Welfare Prohibition Compact 23

Endnotes 27

Executive Summary

“[M]any public officials appear to believe that they can influence the course of their state and local economies through incentives and subsidies to a degree far beyond anything supported by even the most optimistic evidence.”

Alan Peters and Peter Fisher

State policies that advance “economic development,” broadly defined, boil down to government support for businesses through subsidies. These usually take the form of preferential tax treatment, such as select tax credits, or direct grants of taxpayer money to specific firms or industries.

There is broad consensus among academic economists that these programs are wasteful at best and actively damaging to a state’s economy at worst. In addition, they encourage cronyism and corruption by creating high stakes for the winners and losers of such policies.

States engage in these programs to varying degrees of extravagance. A New York Times series of articles compiled a comprehensive accounting of many of these state-based corporate welfare programs in 2012. Though somewhat dated, no such comprehensive accounting has since occurred and there is little reason to believe that much has changed. The Times’ ranking, however, is flawed by the fact that states differ in terms of how they account for these subsidies — some are more transparent than others. As a result, some states may underreport how much corporate welfare they engage in compared to other states with more comprehensive transparency requirements. In addition, the New York Times included some tax provisions that should not be classified as corporate subsidies.

This study ranks the states based on more coherent and consistent criteria which, in particular, includes an adjustment for the size of a state’s economy. That is because subsidies that are large in dollar terms can yield fewer economic distortions in bigger state economies than many smaller subsidies in states with smaller economies. This study’s ranking of a state like Arizona actually places it above high-subsidy states like California and Massachusetts when subsidies are viewed as a share of gross state product. (See page 14 for revised rankings.)

This study applies the logic of public choice economic reasoning to not just the corporate welfare programs themselves but to the political environment in which decisions are made. In so doing, it makes the case for a comprehensive, national solution to break the cycle of unhealthy subsidy competition between states: a “cease fire” or multilateral disarmament agreement — i.e., an interstate compact between states that could finally create momentum toward good forms of tax competition and away from the subsidy-heavy ones. The appendix of this study includes a model compact — the first of its kind — that could be adopted by states.

Introduction

In 2003, Texas Gov. Rick Perry, signed into law something he later trumpeted as one of his grandest achievements: the creation of the Texas Enterprise Fund. The largest of its kind in the nation, this “deal-closing” fund was designed as a tool for state government to provide an enticement to a company looking at Texas as a place in which to relocate or expand. The goal was to use the fund as a final option when Texas competed against other states providing similar viable relocation options for a company. By Sept. 30, 2018, the TEF had awarded about $609 million in grants to 163 different companies.[1] The governor’s office claimed this spending created 94,000 jobs and over $27 billion in investment, an absurd 44-fold return on investment.

Looking at the Enterprise Fund’s records, it is hard to argue that many of the companies that received deal-closing grants would not have chosen Texas as a place to locate even in the absence of the grants. For instance, how likely is it that CITGO Petroleum would not have expanded their refinery facility in Texas without the $5 million TEF grant they received?[2] Oil and Texas are indelibly linked in the public’s imagination for a good reason. Is it really necessary to subsidize a company that likely had few other realistic options for states in which to locate their operations? Nor is it easy to justify the amounts expended for the ability of politicians to declare a victory in the quest for job creation.

The TEF can only claim victory for a miniscule portion of the job creation that occurs in Texas, nearly all of which requires no taxpayer-funded subsidies. Indeed, for 2016 and 2017, the TEF provided taxpayer money to projects that pledged to create a total of 13,041 jobs.[3] Over the same period, the state economy lost 4,392,000 jobs and created 4,736,000 jobs. Even if all companies receiving TEF support created all of the jobs they promised to, the TEF would be responsible for less than half of 1 percent of Texas’ job creation over the period.[4]

Texas is not alone. The 16 companies in Michigan that received deals from the Michigan Business Development Program pledged to create 1,120 jobs in the first quarter of 2018.[5] This is insubstantial compared to the job turnover that happened over the period. The state economy lost 172,700 jobs and added 215,000 jobs. If residents had to rely on jobs programs to drive economic growth, they would find that policymakers would have been able to replace less than 1 percent of the jobs lost in the economy over the period.[6]

A similar phenomenon plays out in all other states. Taxpayer-funded economic development programs are simply not large enough to have a substantial impact on a complex state economy. The massive increase in government resources such a feat would require is not a policy endorsed by corporate subsidy boosters, because even they realize such a large government expenditure — financed as it must be by tax increases or larger debt loads — could wreak havoc with a state’s economy and be extremely politically unpopular, to boot.

This may be why politicians tend to create programs that are — relative to the state’s economy — small in size. Even the small number of highly publicized job programs allows state lawmakers to be a part of photo opportunities when a new plant opens in their district. Deal-closing funds like the Texas Enterprise Fund might best be characterized as “Ribbon-Cutting Funds” — opportunities for politicians to show up and claim credit for a new factory. In other words, these programs don’t improve a state’s economy, but they do help politicians appear as if they are improving the economy.

Meanwhile, other states have tried their hand for decades at favoring certain industries by awarding tax credits and tailored tax exemptions as enticements for new companies to relocate in their state. A five-year-old estimate of the dollar amount of credits and exemptions based in both the personal and corporate income tax code of a state lands at about $228 billion.[7] Indeed, these numbers dwarf the money committed to “deal-closing” funds or direct grants. Tax credits range from those awarded to companies that create “new jobs” — which they likely already intended to create — to those that help underwrite film production.

The latter credit — the film production incentives that many states still have despite recent repeal efforts — is even harder to justify. The film industry is hardly a mom-and-pop business on the verge of bankruptcy. These tax credits, and others like it, simply funnel money to companies and industries that do not need the help, and, in this specific example, largely finance only temporary economic activity in a state — i.e., only the duration of a television or movie production. Most of the real economic benefit is exported to companies and investors outside the state.

Yet, even though these programs are ubiquitous across the country, studies cited in this paper, many analysts and economists, and even some policymakers, acknowledge that states competing against each other in this manner is, at best, a zero-sum game. The best research on the issue suggests these corporate handouts are actually counterproductive, too costly and potentially damaging to the long-term growth prospects of a state’s economy.[8] Confronted with this reality, some policymakers reply with something along the lines of: “We’d love to stop spending time and money on these, but because other states won’t stop, neither can we.” Consequently, these programs survive and state policymakers often continue to feel an urgency to create their own version of these programs in their state.

This study is an attempt to understand this phenomenon and apply the logic of economic reasoning to not just the programs themselves but to the political environment in which these decisions are made. This is not meant to be a comprehensive review of this literature. Instead, the goals of this paper are to provide policymakers, taxpayers and interested members of the public a framework for thinking about this issue and then use it to support a solution — based on today’s political, statutory and constitutional realities — to limit and perhaps even end this unhealthy competition between the states.

What is Corporate Welfare?

The most important question to consider first is how to define “corporate welfare,” a phrase that is often used in discussions of state economic policymaking but is sometimes used too broadly or incorrectly. The Oxford Dictionary definition of corporate welfare is, “Government support or subsidy of private business, such as by tax incentives.”[9] Though a very broad definition, it is essentially correct, although what constitutes “government support or subsidy” is itself up for some debate and often misidentified.

Corporate welfare is any financial benefit purposely granted by government to a specific business or class of businesses and that is not generally available to all businesses and taxpayers. Corporate welfare either lowers the costs of doing business or increases revenue for a business without its customers providing the revenue, relative to other similarly situated businesses, broadly speaking. It might even have both these effects. In short, corporate welfare increases the profitability of a select business or select class of businesses through government action at the cost of other taxpayers.

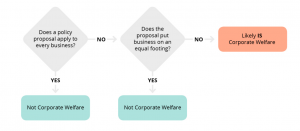

A policymaker can often evaluate if a policy proposal is corporate welfare by asking only two basic questions. First, does the proposal apply to every business in every industry, especially those that are similarly situated? If it does not, does the proposal put the affected business or industry on an equal footing with other similar firms? If the answer to the first question is “yes,” it is unlikely the proposal is corporate welfare. If the answer to the first question is “no” but the answer to the second question is “yes,” it is also unlikely to be corporate welfare, but if the answer to the first and second question is “no,” the proposal is likely to be corporate welfare.

Graphic 1: Determining if a Measure is Corporate Welfare

Examples will be provided later, but the key salient characteristic of corporate welfare is its targeted nature, best characterized as a form of cronyism. This is true even if there is no political quid pro quo, such as a kickback for a favored constituent or campaign donor. Indeed, those types of cases are actually rare. Yet, cronyism in a broader sense should include the softer form in which politicians favor one industry over another, sometimes with the best of intentions, even though doing so has the same economic effect as if kickbacks and straight-up corruption were involved.

The Most Common Types of Corporate Welfare

All states maintain at least one of the types of corporate welfare described here. Many of them offer more than one. Additionally, the federal government has its own versions of many of these programs.

Most examples of corporate welfare policies occur in the name of economic development. Texas once had two substantial funds, the Texas Enterprise Fund and the Emerging Technology Fund, both of which were used to subsidize specific businesses’ expansion in the state. Texas still makes grants through the TEF, although the Emerging Technology Fund, which subsidized high-tech companies, an industry not lacking for investment support, is now defunct. Arizona has its Arizona Competes Fund. Michigan has its Michigan Business Development Program and Good Jobs For Michigan program. Louisiana has the Mega-Project Development Fund. In fact, as of 2014, the New York Times documented that at least 49 states have funds that either provide outright grants or make loans to select companies that operate within their borders.[10]

Grant and loan funds for private business are obvious examples of corporate welfare too. Recipients include large corporations like Samsung, Boeing, Walmart, and General Electric, to name a few.[11] These types of funds are specifically targeted to individual companies on an ad hoc basis and subsidize investments that companies make when they relocate or expand. Besides the promise of local jobs, the primary justification for such actions on the part of a state or city is that other jurisdictions do it and a state would be left out of the competition to host these companies without these programs.

Tax credits and exemptions are often instances of corporate welfare. These can be targeted to a specific industry or they can even be targeted to specific companies. The so-called “angel investment” tax credit is common throughout the country, for example. Investors are allowed to claim credits against investments they make in specific companies, often small businesses, that government has approved or certified in some way. This subsidizes a business’s capitalization. Credits might be federal, state or local in origin, and they are usually applied against income taxes, but there are property tax credit programs as well.

Another type of corporate welfare occurs when government makes nontraditional, extraordinary investments. Sports stadiums are often financed and sponsored through local governmental entities such as special districts or public corporations that receive dedicated tax receipts from hotel and rental car taxes as well as through local property tax money. Technology companies have benefited from government investments in fiber optic and cable installations. Industrial parks sometimes see governments financing facilities not open to common use, like buildings, that are not part of a community’s general infrastructure and are not traditionally financed by government.

Deal-closing funds and grants

At least 34 states make outright monetary grants of some sort to companies that locate or expand within these states’ borders. The most common type of grant reimburses companies for expenses incurred in training employees. Another type of grant, usually based on a formula, compensates companies when they meet employment-related criteria, such as employing a minimum number of individuals or paying a certain wage. This type of direct grant program is much less popular with business, however, partly because the benefit for meeting such criteria is usually handed out in the form of ex-post tax credits and exemptions instead of up-front payments.[12]

An increasingly popular form of a grant, both for business and government, and perhaps the most wasteful, is the discretionary deal-closing fund. Discretion is usually exercised by a state’s governor or an individual or committee appointed by the governor. These funds are often handed out using an undefined and nontransparent process, and for often undisclosed purposes, to large corporations to induce them to locate facilities within a state. Twenty-two states have deal-closing funds.[13] The aforementioned Texas Enterprise Fund is one example of these types of programs.

Deal-closing funds are especially damaging because of the likelihood that grants will be handed out purely on the basis of political influence rather than on any objective criteria, even when seemingly objective criteria are specified in law. All grants, like any corporate welfare, are potentially economically distortive, but discretionary grants are especially so as they substitute arbitrary and political decision-making for market forces, enriching a few at the expense of many. The costs of these economic distortions exceed the apparent taxpayer expense of these grants. States’ grant programs vary in their eligibility requirements, but when the supply of funding is exceeded by demand, discretion must be exercised; it is not likely to be entirely objective, nor are the requirements that might be written into law.

Professional sports are also often singled out for subsidy, more often at the local level. The subsidies are largely aimed at stadiums, which are often financed in part by bonds that are partly paid by local taxes. The share of financing varies from project to project and examples are too numerous to list here, but most professional sports forums have at least some share of public funding, which amounts to an outright grant of wealth to the owners of professional sports franchises.

There are other corporate welfare grant funds that are often overlooked, such as by the New York Times in its catalog of these programs. For example, Arizona has a Biomedical Research Commission, with its own dedicated revenue source. It funds research by private corporations in addition to that by academic and nonprofit institutions.[14] Maine and Florida have similar funds.[15] Oklahoma directs some tobacco settlement funds to health research through its Tobacco Settlement Endowment Trust.[16] Texas funds cancer research through the Cancer Prevention & Research Institute.[17] Michigan operated a number of business plan competitions that handed out grants and loans to winners.[18] These examples are in addition to the many millions states spend indirectly on research that benefits various industries and specific companies by funding universities.

Tax preferences

Tax preferences are a category of subsidies provided through the tax system and can come in a variety of forms. Each of them provides a specific industry or company a tax benefit by either exempting them from certain types of taxation or by allowing a company to pay a lower tax than a company that is similar in all or most respects except for the fact that the government chose not to subsidize it through preferential tax treatment.

As noted previously, tax preferences should not be confused with broad-based tax policies that result in lower general tax rates. Broad-based policies apply equally to all businesses and can be utilized by any company that has tax liability. Examples of broad-based tax policies are the lowering of general business tax rates and creating tax deductions and exemptions that most businesses could benefit from. Preferential tax treatment, on the other hand, only impacts specific businesses, usually those that have been deemed by politicians or bureaucrats to be critical to the local or state economy or deemed necessary to meet some other policy goal.

Tax credits directly reduce the amount of taxes that a company owes. They are often awarded to a business that undertakes a specific activity, such as an expansion of their operations or the creation of a specific number of new jobs in a state. Tax credits are usually designed to favor a specific type of company, i.e. those operating in a certain type of industry or in a certain location.

Tax credits can also result in direct taxpayer-funded subsidies to companies, when credits exceed the company’s tax liabilities and the credits are made refundable. Other credits are transferrable, and allow the businesses that earn them to sell the credits to other businesses.

An enterprise zone is a preferential tax policy intended to lure companies to a specific geographic area within a state through a lower tax burden for the relocated company facility. If a company locates in one of these zones — some of which may, but not necessarily, be in blighted urban areas — they can receive favorable tax treatment, such as property tax abatements or lower effective tax burdens on other taxes, such as a corporate income tax. This policy was originally proposed by Jack Kemp as a way to demonstrate the economic strength of an area with limited government and low taxes.[19] The limited government part has been entirely neglected with the policy now morphed into a special privilege scheme for supposedly blighted areas.

A close cousin to enterprise zones, tax increment finance districts, or TIFs, redirect a portion of taxes owed to a polity by the taxpayers in a defined region. When a TIF is designated within, say, a city, the taxes that would be generator for the city’s general fund from a particular district are limited for a time, often for multiple decades. The tax revenue generated from this district that exceeds what is owed the city can then, in some cases, be used for corporate welfare. The result is a small area relatively rich in collective resources that often give it a competitive edge, especially in places like Oklahoma where districts can only be created by cities and counties, but can access school property taxes.[20] In some cases, ostensibly for blighted areas, TIFs are sometimes applied to just a single property.

Property tax abatements are offered by some localities or states for specific businesses and industries. They are a way of offering lower property tax rates for certain properties. These tax incentives impact other property taxpayers who are not able to receive the same favorable property tax treatment in a very direct way. Because the property tax base of a locality — which often is tethered to a specific set of budget categories, such as school funding — is subsequently reduced as a consequence of these property tax abatements, it could have the effect of increasing property taxes for everyone else, higher than they otherwise would be. In some cases, this situation may also result in an actual tax increase on nonfavored property owners. Abatements in Texas, which can be forthcoming from school districts, are a close cousin to TIFs since abatements only occur within designated “reinvestment zones” and are limited to 10 years. In Fort Worth, abatements have been granted to corporations like Coca-Cola, American Airlines, Bell Helicopter and Blue Cross Blue Shield.[21]

Finally, sales tax exemptions exclude certain categories of goods or certain transactions from all or a portion of state sales taxes as a way to encourage a business to relocate to a state. In some cases, some part of sales tax collections is refunded to the businesses that collect them as an incentive for those businesses to locate in a specific area. Such arrangements would likely be most attractive to larger companies that would have a substantial sales tax burden otherwise, such as large retailers like Walmart or other big-box chains. Of course, the sales tax burden is actually paid by customers, and it is their tax remittances being returned to these retailers. In Arizona, such arrangements have been judged to run afoul of the state’s “gift clause” — a prohibition on government granting gifts to corporations.[22]

In some states, calculations of foregone revenue performed by legislative budget offices and departments of revenue would rank sales tax exemptions as much more generous than the direct grant programs that those states offer. Many of these calculations, however, include exemptions for such items as plant equipment. This is actually just good tax policy since it prevents “tax pyramiding” (explained more fully below) and should not be considered corporate welfare or even a tax exemption.

Lending programs

Businesses frequently must borrow in order to make major investments, especially as they are initially organized and begin operating. This entails risk for lenders, especially in cases where loans are requested by businesses that are untried and new. Nevertheless, the market can and regularly does provide this start-up capital. For example, venture capitalists often provide funds in exchange for ownership interests in companies. Cosigners can provide collateral for loans, as do second mortgages.

Despite these private methods of borrowing funds, state and federal governments, individually and in concert, often offer businesses, especially small businesses, guaranteed loans, on terms not unlike those offered to college students. For a lender, a government loan guarantee reduces risk, in some cases all the way to zero, because the government promises to repay the loan if the borrower defaults. From a big-picture perspective, guaranteed loans represent a very real subsidy to banks that participate, since these guarantees lower their costs of doing business.

Loan guarantees are also an obvious subsidy to the businesses who receive the loans. Since the loans are artificially made relatively low-risk to the lender, less interest is charged on the loan, benefiting the borrower. For that matter, the borrowing business might never even have gotten the loan but for the guarantee. Given the scarcity of loanable funds, businesses that participate in loan guarantee programs crowd out other potential business borrowers who do not participate in a guaranteed loan program. This gives a distinct competitive advantage to the businesses that participate.

The federal government is the largest provider of guaranteed loans through three major programs. The U.S. Department of Agriculture provides guaranteed loans through a program meant to support rural small businesses.[23] The U.S. Treasury Department runs the State Small Business Credit Initiative, with another $1.5 billion in funding. This program uses state-level go-betweens in 47 states. Alaska, North Dakota and Wyoming do not participate.[24] State participation in both of these programs is decidedly uneven. Wisconsin has received, by far, the largest amount of funding under the USDA program. California is the biggest recipient of Treasury’s program. Georgia gets more funding under both programs than Texas does, although Texas’ shares are significant. Less information is readily available regarding the U.S. Small Business Administration’s guaranteed loan program, referred to as the “7(a) Loan Program.”[25] However, there is little doubt that participation is uneven, likely reflecting variation in the sophistication of various SBA state offices.

Some states have their own guaranteed loan programs, sometimes narrowly tailored to favor minority-owned businesses or agriculture. All are justified on the basis that they help to create jobs. And, no doubt, there are jobs associated with the businesses these programs have helped. On the other hand, loanable funds are scarce and funds going to these businesses are denied to others. It’s much harder to point to jobs that have not been created due to these programs, but this is, in fact, the case. Whether the net is positive or negative can be debated, but since market participants tend to scope out the best available productive alternatives for investing funds, and these programs interfere with that process, the result of these programs is likely an overall net negative to society as a whole.

States also go beyond loan guarantees and make direct loans to select companies. Select companies have received loans from Michigan’s Jobs for Michigan Investment Fund. State auditors note, “These are high-risk loans issued for the purpose of diversifying Michigan’s economy and helping to create jobs in competitive edge technologies.”[26]

Investment Programs

States have setup funds to directly invest in companies. Michigan’s 21st Century Jobs Fund partnered with a number of venture capital, private equity and mezzanine lending firms to invest for economic development purposes and also have a chance to provide returns to taxpayers. These give businesses access to capital that they may not otherwise have and reduces pressure from investors to provide returns.

What is Not Corporate Welfare?

Knowing what should not be regarded as corporate welfare may be even more important for a policy discussion than knowing what should be. Some tax provisions, though often viewed as corporate welfare, are often consistent with economically efficient tax policy and should not be viewed as welfare.

Some sales or property tax exemptions of certain goods or services and some broad-based income tax provisions are sometimes viewed as subsidies. Take sales tax exemptions for business inputs as an example. Taxing raw materials that go into a manufacturing process is a form of double taxation. If each stage of production of a good were taxed the same as the final purchase of that good, taxes would be charged on taxes, distorting the true costs of production and efficient market prices. While it may seem unfair that a certain type of good or service is exempt from taxation for a business when it is taxable to an individual, this does not automatically make the exemption a subsidy.

Another example of good tax policy sometimes mistaken for a subsidy is the ability of a company to more quickly deduct the cost of its investments. In a perfect world — one in which the tax code did not distort market decisions — businesses would be allowed to deduct their capital purchases immediately in the same tax year they were made. However, current law requires investment costs to be netted out of income over a period of years (i.e., depreciate them). This can be too long a period to fully expense investments once inflation is taken into account.

Some states and the federal government have accelerated the timeframe within which businesses can depreciate. Some small businesses today can even instantly write-off (i.e., expense) all the capital purchases made in a single tax year below a certain value threshold. Compared to the status quo, this might seem to an uninformed observer like a subsidy to a business since accelerated depreciation and instant expensing result in a lower tax bill for a company relative to the status quo baseline. Actually, it is just good tax policy and corrects a flaw in the tax code.

Some tax disparities may exist as a natural consequence of the evolution of a marketplace or industry, not because of legislative activity or policy changes. Amazon, Wayfair and other internet-based companies, like catalog companies before them, have benefited from not having to collect sales taxes from their customers to then be remitted to their customers’ respective states.[27] However, this was not corporate welfare. It might have been unfair from the perspective of other retailers that did not operate across state lines and sell over the internet. It was arguably economically inefficient and distortionary. Amazon and Wayfair’s advantage, though, was not a result of concerted government action intended to provide them special treatment. It was accidental, and even though these internet-based companies actively sought to keep that advantage, federalism complications are such that legislative inactivity does not amount to action that can be considered corporate welfare.

What’s So Bad About Corporate Welfare?

Given the economic development and job creation justification for most corporate welfare schemes, it would be natural to wonder, What is so bad about it? After all, most people would agree that job creation through job training and investment is a good thing. The fundamental issue, though, is whether corporate welfare results in efficient market outcomes in terms of jobs and investments, based on the actual resource costs and productive benefits. For example, the federal government heavily subsidizes the ethanol industry, but this has led to heavy water use to grow corn for ethanol production instead of for food and animal feed. This has, in turn, led to higher food costs than would have existed otherwise. Likewise, state and local subsidies distort economic outcomes leading to inefficiencies that, in total, can be quite significant.

Because corporate welfare programs, whether in the form of grants, loans, or favorable tax treatment, are determined by political forces to advantage certain types of businesses or economic activity, distortions are created in the marketplace by favoring one type of capital category or business model over another. The success of such a strategy is severely limited by government’s inability to make the best use of knowledge about the potential future winners in the marketplace.[28] Some industries, such as solar and wind power generation, Hollywood productions and professional sports, have received a good deal of favorable attention from government. Yet, there is no certainty that these investments will ultimately become cost effective. If they never do, government will have encouraged endeavors that demonstrably result in more costs than benefits, and therefore are a waste of finite investment resources.[29]

Empirical studies produced by professional economists indicate that government isn’t better than the market at either picking winners in the marketplace or at encouraging job growth. For example, a recent study looked at the Kansas tax credit program Promoting Employment Across Kansas, or PEAK. The study took a unique approach to determining the effectiveness of the program by surveying the natural experiment taking place in that state. It compared companies with similar attributes except for one: whether they received a PEAK job creation tax credit or not. Nathan Jensen of the University of Texas-Austin, the author of the study, concluded that companies that received PEAK tax credits were not statistically any more likely to create new jobs than similar firms that did not receive the subsidy. Additionally, the PEAK recipient companies had little impact on job creation in the state because they were simply no more dynamic in the creation of new jobs compared to the nonsubsidized control group.[30]

This is consistent with the weight of empirical analysis on this subject. A comprehensive 2004 article in the Journal of the American Planning Association by Alan Peters and Peter Fisher of the University of Iowa comes to a conclusion that has since largely become the consensus among academic economists. After reviewing a wide body of articles and cost-benefit analyses on economic development programs — which included multiple tax credit programs and enterprise zones — they conclude that “there are very good reasons — theoretical, empirical, and practical — to believe that economic development incentives have little or no impact on firm location and investment decisions.”[31]

Peters and Fisher go further to state what likely drives support for these programs. They suggest:

The most fundamental problem is that many public officials appear to believe that they can influence the course of their state and local economies through incentives and subsidies to a degree far beyond anything supported by even the most optimistic evidence. We need to begin by lowering [policymakers’] expectations about their ability to micromanage economic growth and making the case for a more sensible view of the role of government — providing the foundations for growth through sound fiscal practices, quality public infrastructure, and good education systems — and then letting the economy take care of itself.[32]

An almost tragic example of how corporate welfare can backfire comes out of Arizona. In 2008, the state Legislature passed a measure creating an amusement park district that would have essentially zeroed out sales taxes for an amusement park constructed under that law. Ostensibly, the law was passed for a rock-and-roll themed amusement park proposed for an area near Eloy.[33] Within a year of the measure’s passage, the entity supposedly developing the park had gone bankrupt.

In the meantime, long-time Arizona resident and independent businessman Dan Stokich, prior to the amusement park district law’s passage, was on the cusp of assembling the financial investors necessary to build a large amusement park on a Disney-like scale. Because his marketing consultants’ studies indicated Eloy was unsuitable for such a project, he would never have taken advantage of the amusement park district law. At the same time, despite the unlikelihood of the rock-n-roll themed park’s success, the Arizona Legislature’s action introduced enough additional risk for Stokich’s investors that they backed out altogether. To this day, Arizona has no major amusement park, and there is evidence that the Eloy proposal and a more recent one that materialized after the Eloy law’s expiration only existed as distractions to block legitimate efforts like Stokich’s.[34]

Other examples of crony economic development schemes that have backfired just from Arizona include speculative deals involving the issuance of bonds to attract private enterprises to specific locations. The cities of Gilbert and Peoria have issued bonds to support construction for the benefit of private colleges, only to see what they thought were promising enterprises ultimately shuttered.[35] Pima County issued bonds for the sake of a high-altitude, balloon-making company that is unlikely to ever have more than a handful of employees.[36]

Corporate welfare also distorts healthy private capital markets because it makes the targets of the subsidy more attractive to investors than they would be otherwise. Investors in the subsidy-receiving companies would anticipate a higher rate of return or less risk than they might otherwise since costs are effectively reduced by the subsidy. Consequently, more investment flows to the companies that take advantage of corporate welfare opportunities. This might be appropriate if government officials possess a clearer vision of how such investments will fare in markets, but there is no reason to believe this is the case. In fact, it is far more likely that government officials substituting their limited judgment for the market’s collective judgment will result in a less than optimal outcome with too much investment in government’s arbitrarily favored industries.

Corporate welfare also encourages economic waste while simultaneously encouraging corruption or its close cousin, cronyism. Businesses and industries expend resources vying for various types of subsidies — which by definition are economically inefficient as these are resources that could otherwise be used to invest in more productive ventures. Others who are their competitors might expend resources in an effort to fight against prospective subsidies, which furthers — indeed potentially doubles — the economic waste of resources dedicated to lobbying efforts.

Elected and appointed officials get courted by interests seeking profit by any means and can often be misled about the efficacy of their decisions. This creates an environment fertile for outright corruption such as bribery, or the softer corruption of susceptibility to suggestion from lobbyist friends who have carefully cultivated relationships with policymakers. And it also creates opportunities to exchange favors to select interests for employment opportunities for outgoing legislators and their friends. In any case, the more favors government officials can hand out to select interests, the higher the stakes for these interests to command a politician’s favor.[37]

Finally, businesses and industries that receive corporate welfare take greater risks than they might otherwise because risk is more affordable and is usually imprudent relative to market realities. A sizable portion of solar companies that have been subsidized at multiple levels of government have gone bankrupt.[38] This could be partly due to risks being taken that otherwise would not have been taken had corporate welfare subsidies not been handed out. These are wasted scare resources that should have been put to more efficient use.

Ranking the States: Improving the New York Times

Corporate Welfare Ranking

In 2012, the New York Times released a database of corporate subsidies from state and local sources, a largely comprehensive list organized both by company and state program. This list includes programs used to transfer money, services or tax benefits from government (i.e., taxpayers) to companies.

There are two major, related flaws in the New York Times’ worthy effort, though. The Times’ major flaw is assuming that all sales tax exemptions are an example of corporate welfare when, in fact, many are justified economically. In addition, states that transparently and fully report the full value of exemptions, whether or not they are economically justified, see their degree of corporate welfare largesse artificially bloated compared to those less transparent.

Texas deserves criticism for its corporate subsidy largesse. However, the New York Times exaggerates Texas’ ranking due to the ready availability of data on the value of sales tax exemptions. Thus, in effect, the Times penalizes Texas for being more transparent. For example, nearly every state offers a manufacturing equipment sales tax exemption — a justifiable tax exemption on economic grounds — but only a few states report the value of that exemption, as Texas does. The same applies to Michigan, where the Times considers the state’s sales tax base on retail goods to be a subsidy for businesses that provide services.

The manufacturing equipment exemption is good tax policy because it is an attempt to restrict taxes to the final item sold. This avoids “tax pyramiding,” which occurs when inputs to production are taxed as if they were a final-use good for purchase. By the time the product reaches the consumer, taxes have been applied to taxes and priced into the good. This not only inflates taxes, it also renders them largely invisible to taxpayers. The sales tax that is then applied to a consumer’s purchase results in multiple layers of taxation.

As an example, in most states there is an exemption for cars purchased by rental companies. This is because each time the car is rented, the renter pays the sales tax. If there were no exemption, the renter would effectively pay a double sales tax due to higher charges to cover the initial higher cost for the car rental company of acquiring the vehicle. The same reasoning applies to manufacturing equipment or other inputs. The exemption is not given to profit the companies, but to keep consumers from being taxed twice and to prevent market distortions since products with more stages in the production line are disadvantaged relative to those with fewer stages.

Preventing double taxation is not a form of corporate welfare. Instead, it produces a tax system that is simpler and more transparent by enabling the end user to easily calculate how much tax they are paying on the final good. It also avoids the economic distortion that would come from a tax system encouraging fewer firm-to-firm transactions at stages of production simply to avoid a bigger tax hit. Taxing every stage of production when transactions occur between firms encourages vertical integration as a tax avoidance measure rather than as a true efficiency-enhancing measure.

Our analysis indicates that about two-thirds of the subsidies reported by the New York Times are not truly subsidies; they are actually appropriate elements of tax structure designed to make taxes more efficient and prevent double taxation. These “fake subsidies” include elements such as “freeport” exemptions and accelerated cost recovery systems for equipment and S-corporation write-offs. Many states also have an exemption from the corporate income tax for S-corporations.

Taking the New York Times data and removing the entries that are not truly subsidies, we have constructed a new ranking based on what we belief to be a more consistent definition of corporate welfare. Additionally, instead of ranking states based purely on the dollar amount of the subsidies as the New York Times did, our ranking is based on the size of the subsidies as a percentage of gross state product. This gives a better indication of how distortionary the subsidies may be in each state — large dollar amounts for subsidies may not matter so much in Texas, already a large economy, than they might in Kentucky. This creates a better perspective of the role corporate welfare actually plays in each state and the size of the economic distortions they create in each state.

Included in our ranking are cash grant programs like the now-defunct Texas Emerging Technology Fund and bond issue programs or free services given to companies. Also included are exemptions granted to companies targeted specifically at benefiting one company or a small group of companies, such as exemptions or tax breaks for small businesses.

Graphic 2: Revised State Corporate Welfare Ranking

| Rank | State | Subsidies Per GSP |

NYT Ranking | Rank | State | Subsidies Per GSP |

NYT Ranking |

| 1 | Alaska | 1.36% | 25 | 26 | Pennsylvania | 0.09% | 3 |

| 2 | Kentucky | 0.74% | 16 | 27 | Florida | 0.09% | 5 |

| 3 | Louisiana | 0.41% | 21 | 28 | Illinois | 0.08% | 14 |

| 4 | Michigan | 0.36% | 2 | 29 | Maryland | 0.07% | 28 |

| 5 | Hawaii | 0.34% | 37 | 30 | Wisconsin | 0.07% | 13 |

| 6 | New Mexico | 0.30% | 38 | 31 | Arkansas | 0.07% | 31 |

| 7 | Texas | 0.29% | 1 | 32 | South Dakota | 0.07% | 50 |

| 8 | South Carolina | 0.27% | 30 | 33 | Mississippi | 0.06% | 32 |

| 9 | Oklahoma | 0.26% | 10 | 34 | Delaware | 0.05% | 46 |

| 10 | Montana | 0.25% | 43 | 35 | Ohio | 0.05% | 7 |

| 11 | Washington | 0.25% | 8 | 36 | Georgia | 0.05% | 17 |

| 12 | West Virginia | 0.21% | 12 | 37 | Colorado | 0.05% | 42 |

| 13 | Oregon | 0.20% | 23 | 38 | Maine | 0.05% | 29 |

| 14 | New York | 0.20% | 6 | 39 | North Carolina | 0.04% | 27 |

| 15 | Nebraska | 0.20% | 18 | 40 | Virginia | 0.04% | 19 |

| 16 | Rhode Island | 0.18% | 34 | 41 | North Dakota | 0.04% | 49 |

| 17 | Arizona | 0.18% | 15 | 42 | Missouri | 0.03% | 44 |

| 18 | Vermont | 0.17% | 33 | 43 | Minnesota | 0.03% | 39 |

| United States | 0.13% | 44 | New Hampshire | 0.03% | 47 | ||

| 19 | Connecticut | 0.13% | 24 | 45 | Wyoming | 0.03% | 45 |

| 20 | New Jersey | 0.12% | 26 | 46 | Indiana | 0.03% | 22 |

| 21 | Iowa | 0.12% | 40 | 47 | Tennessee | 0.03% | 11 |

| 22 | Alabama | 0.12% | 36 | 48 | Nevada | 0.03% | 48 |

| 23 | California | 0.11% | 4 | 49 | Utah | 0.02% | 41 |

| 24 | Kansas | 0.11% | 20 | 50 | Idaho | 0.01% | 35 |

| 25 | Massachusetts | 0.10% | 9 |

As can be seen in Graphic 2, once the value of economically justified tax exemptions are removed from the New York Times data and a calculation is made relative to gross state product, the rankings radically change. Texas, still a corporate welfare standout, ranks seventh instead of first. New York falls from sixth according to the New York Times ranking based on absolute value, to 14th. Alaska jumps up from 25th to first. Kentucky, Louisiana, Hawaii, New Mexico and South Carolina see similar jumps in ranking.[39]

Arizona and Oklahoma do not budge much in the revised rankings. However, it’s important to note that our revised ranking actually places them both above California and Massachusetts — two states notorious for trying to micromanage their economy via government policy and business subsidies. Michigan, along with Texas, remains a corporate welfare standout even after the rankings are adjusted. These are only a few examples of how the rankings are impacted by properly accounting for corporate welfare.

An Alternative to Subsidies: Healthy State Competition

Justice Louis Brandeis is famous for having characterized the various states as policy “laboratories.” Although Brandeis likely did not intend his words the way they are often interpreted, the fact is that states do have a great deal of autonomy over taxes, regulation and spending.[40] In addition, each state has, at least to some degree, its own culture that feeds back on its institutions and policy choices. These characteristics combine to create an overall climate for business, arts, education and other endeavors. While states should not enter into head-to-head contests to attract specific businesses or industries by singling them out for special privilege, the states can and should pursue general policies that promote a vibrant economy and community.

There are at least three dimensions on which competition between states can thrive that are healthier than the current obsession with subsidies.

Regulatory Competition

States already compete in the regulatory arena, even if state policymakers fail to take account of it. Think tanks regularly publish studies of economic freedom in the states that have a regulatory component.[41] Forbes magazine publishes a ranking of states in terms of their business climates and one of the criteria has to do with regulation.[42] Chief Executive magazine does the same.[43] No doubt, there are other examples, not to mention word-of-mouth among those who make facility placement decisions for large companies.

States’ regulatory regimes differ for a variety of reasons, and some regulation might be inevitable, depending on the specific circumstances in which a state might find itself. For example, Los Angeles essentially sits in a half-bowl formed by mountains to its east while prevailing winds blow from the west. Therefore, pollution is a particularly big problem there because it does not blow away. Naturally, more stringent atmospheric emission regulations might be more justified there than elsewhere.

Not only is it legitimate for policymakers to think carefully how their choices affect their state’s business environment compared to others, it is incumbent on them to think carefully how their regulatory rules affect their state’s business environment compared to others. A law passed in response to circumstances that might best be addressed through civil action, better information or the assumption of risk could have long-lasting, negative economic consequences for a particular state.

Chambers of commerce and various levels of government that have little to no direct control over regulations imposed by other levels of government can still take action to minimize regulation’s impacts. Regulatory specialists can become expert in learning about regulation and can become acquainted with specific regulators so as to facilitate businesses’ meeting regulatory requirements. Such experts can also serve as advocates for the business community, questioning the need for regulation and making recommendations to streamline regulatory compliance. By establishing regulatory “clearinghouses,” state and local governments can reduce the need for every business to replicate other similar businesses’ knowledge of regulatory requirements and reduce the time and cost involved in meeting regulatory burdens.

Cultural Competition

Every state has its own culture that policymakers are hard pressed to impact. Nevertheless, states do compete on this basis. Policymakers do have the bully pulpit, though, and can help to focus efforts toward greater business friendliness. Houston has repeatedly voted down efforts to establish a zoning regime. Policymakers there play a part in both promoting zoning and fighting it. Zoning is regulation that does as much or more to inhibit and redistribute to the politically connected as it does to protect property rights. Houston has demonstrated a culture friendly toward business as a result of rejecting zoning regulations.

San Francisco, on the other hand, has generally demonstrated a culture of hostility toward business with its stringent zoning and development restrictions. The city continues to do well economically because of its natural, geographically-based advantages. On the other hand, San Francisco is home to two upstart ridesharing services, Uber and Lyft, which have often been under fire from regulators in various states, including some considered business-friendly.

For the most part, elected policymakers will tend to reflect the wider culture. However, to the extent that they are truly community leaders, they can gently and marginally impact the mood of the wider community and help it to compete for businesses in search of a welcoming home.

Tax Competition

While subsidies should be dismissed as a means of unhealthy competition, this does not mean that there are no grounds on which states may compete on tax policy. On the contrary, the grounds for competition are more fertile without corporate welfare in the mix.

States can compete on rather traditional grounds of having the lowest tax rates for all companies and individuals. Even-handed property tax policies that don’t penalize specific types of property (whether through selective higher tax rates or by creating exemptions for specific types of property but not for others) are also important.

Competition between states on the proper kind of tax base is also critical. In fact, states that do not have an income tax are competing on exactly this sort of dimension: they are committed to taxing the consumption in a state, not the investment or income-production in a state. States, therefore, can generate new economic activity simply by transitioning to a more investment-friendly tax base even if tax rates or tax collections remains the same. Tax credits that create a more investment-friendly climate for some and not for others suffer all of the economic distortions that have been discussed already. A neutral and investment-friendly tax climate, on the other hand, benefits all.

Reining in Corporate Welfare

What follows is a recommendation to make corporate welfare more difficult to implement or, hopefully, eliminate it altogether. It is a proposal for comprehensively removing a major incentive to grant corporate welfare — destructive, mercantilist competition among states within the United States.

Achieving Healthier State Competition with a “Cease-Fire” Agreement

Even if it is generally accepted that competition between states to see who can dole out more subsidies is an unhealthy form of state competition, action is not easily taken. Careful consideration must be given to what reforms might be taken, particularly in the context of today’s political environment in which states are encouraged to compete in this deleterious way.

An immediate and obvious solution for a state is to simply stop handing out subsidies. But the political gain to be had by handing out a subsidy, which allows policymakers to take credit for a company relocating to the state or an expansion of an existing facility — even if the subsidy had nothing to do with it at all — is hard for any policymaker to resist. This is because the opportunities that are foregone because the subsidy was awarded — the capital investment that did not happen in a company that did not receive the subsidy or a job that was not created somewhere else in the state — remain unseen by the public at large. This is true although the economic benefits of lost opportunities are likely larger than the benefits that result from the subsidy, resulting in a net loss. In the end, the opportunity for good press for a policymaker trumps all the net negatives of a bad policy.

Due to the political calculus just described, it is difficult for any coalition of policymakers to “unilaterally disarm” their state in the subsidy battle even when there are demonstrable benefits to doing so. If a group of states decided to simultaneously disarm, on the other hand, then as long as all could make a credible commitment not to renege on the deal, everyone would be better off. This is what is known in game theory economics as a “collective action problem.” Every player would be better off with the outcome in which everyone was disarmed, but nobody is willing to make the first move in that direction for fear that they would be worse off if other players do not follow suit.

This same collective action phenomenon exists with international trade. The government of a nation can capture the political benefit of sheltering a particular industry with trade barriers, usually in the form of tariffs on imports, even though citizens of all nations would benefit from free trade with low or no tariff barriers. A high tariff on a good benefits that good’s producers in the nation with the tariff because other countries’ product are made artificially more expensive for consumers in the tariff-imposing country.

If states were able to charge tariffs against other states, they could do so in the name of protecting and developing homegrown industries and jobs. In a very real sense, giving tax preferences and subsidies to certain companies but not others is a form of trade barrier not unlike tariffs. Instead of favoring an industry by increasing costs for its competitors, states artificially lower costs for the industry that locates within its borders. Just as a tariff favors one good or industry over another, so do state government grants and tax subsidies.

The authors of the U.S. Constitution were quite aware of the problems inherent in states erecting barriers to trade between them. It was a very real problem during the period of the Articles of Confederation when states sometimes charged tariffs on goods purchased from other states or imposed tariffs on imports that crossed their borders but were purchased in other states. At the time, states could erect their own tariff barriers against international imports, especially from Britain. Citizens could get around these by buying the same goods from other states with low tariffs, so state-to-state trade barriers were erected.

This problem was ultimately solved through the Commerce Clause in the U.S. Constitution, which gives Congress the exclusive power to regulate commerce among the states. Congress quickly enacted prohibitions against state-to-state tariffs after ratification of the Constitution. In so doing, they created the geographically largest free trade zone at the time. This policy contributed to the rapid economic rise of the United States because states could economically specialize according to economic realities and real innovations, uninfluenced by artificial costs like tariffs.

In international trade, collective action problems related to tariffs have been solved to some degree through bilateral and multilateral treaties between nations, the conditions of which require the lowering of trade barriers. Enforcement mechanisms for such treaties range from fines issued from an international adjudicator — in this case, the World Trade Organization — or by a “countervailing duty” which is a tariff that can be imposed on the imports from a nation that has been proven to violate the terms of the treaty or agreement. No matter how the treaties are structured, they all have the same goal: to make free trade the default policy, not the exception.

The same mechanism and logic can apply to a “cease-fire” agreement between the states concerning corporate welfare. Interstate compacts (contracts between states that are allowed under the constitution) could reboot healthy competition between states and codify a discontinuation of corporate welfare subsidies, especially those intended to further one state’s economic interests over another’s.

A compact in and of itself may not completely solve the collective action problem, since no one state or small number of states will agree to end all corporate welfare subsidies while others continue to offer them. To encourage states to join the compact, it must contain within it a provision prohibiting compacting states from competing with each other through corporate welfare schemes. However, compacting states could still compete in this way with states that have not entered the compact.

It’s also important to note that this compact would have built into it a provision that could be described as a “we jump when we all jump” provision. That is to say the cease-fire would only kick in when a threshold number of states enter the compact. Not only will this create a bigger “free trade zone” within the compact and consequently increase its likely effectiveness at achieving the desired results, but it would also avoid what may be called the “chump problem” — a situation in which only a few states join the compact, but because the provisions are in force immediately, feel like chumps for doing so. This increases the likelihood of those states terminating the compact and extinguishing the promise such a compact could provide over the long term.

In order to end nearly all corporate welfare that acts like barriers to trade, all states would have to be prohibited from doing so through an act of Congress under authority of the U.S. Constitution’s Commerce Clause. To accomplish this, the compact could contain a trigger that activates it when enough states have signed on to constitute a three-fifths majority in the House and Senate, enough to ensure a successful cloture vote in the Senate. The trigger could prohibit all compacting states from handing out corporate welfare, regardless of what nonsignatory states do. This would create an immense pressure on a significant majority of Congress to exercise its legitimate constitutional duty and legislate a stop to corporate welfare competition between the states. With this formulation, states could adopt the compact without concern that it will kick in for a little while, which solves a potential hurdle to adoption by a state.

Congressional action to short circuit the sorts of unhealthy state competition outlined in this study could still occur even in the absence of a compact. Action by the courts could also resuscitate the U.S. Constitution’s Commerce Clause. For instance, a 2004 decision by the Sixth Circuit in the case of DaimlerChrysler v. Cuno struck down a tax credit that allowed the expansion of their facilities in Ohio as a violation of the Commerce Clause because it, by definition, discriminated against interstate commerce.[44] That decision made a very strong statement that what legal scholars refer to as the “dormant Commerce Clause” would preclude such a tax credit because it had the effect of favoring in-state expansion over other types of economic activity that might involve movement of capital and jobs to another state. Unfortunately, the U.S. Supreme Court negated the applicability of this decision after it ruled that claimants lacked standing necessary to bring their case.

Because states do not have a viable way to register their preference for a cease-fire in the state subsidy war, there is little incentive for Congress to act or for states to discontinue their subsidy activities on their own individually. The mechanism of a state compact would provide such a way to not only register this preference — which is made possible because each state could be assured others would eventually follow suit — but also send a message to Congress that they must reassert their power to legitimately regulate commerce between the states in a way that benefits all through the Commerce Clause power. A state compact that has built within it an activation trigger that kicks in when a specific share of the population is covered by it would provide the signal necessary for members of Congress to understand that it is politically possible — indeed, perhaps even vital — for Congress to put a stop to discrimination against interstate commerce.

One objection to the proposed compact is that Article I, Section 10 of the U.S. Constitution stipulates that states need congressional consent to create compacts. This consent, however, according to nearly 200 years of Supreme Court case law, can be provided after the compact is created and can be done so implicitly.[45] In addition, legal precedent has established that congressional consent is not necessarily needed if the interstate compact does not impact the delegated powers of the federal government.[46] The proposed interstate compact would avoid this pitfall because it would only exercise the member states’ own sovereign control over its taxing and spending policy.

The appendix of this study includes a draft of a compact proposal that would satisfy the characteristics just discussed. Its major provisions are as follows:

- Tightly defines corporate welfare subsidies and prohibits compacting states from engaging in such competition with each other.

- Provides that any compacting state may withdraw at any time prior to the supermajority congressional provision being satisfied, but prohibits withdrawals after the satisfaction of the supermajority provision.

- The governor or the governor’s designee of a compacting state is obligated to:

- Keep an up-to-date list of all compacting states,

- Maintain and provide any documentation to other compacting states necessary to administer the compact, and

- Communicate to Congress that it should act to prohibit corporate welfare at the state and local levels when a trigger number of states has joined the compact.

- Requires the chief law enforcement officer of each state to enforce the compact and allows a private citizen standing to sue to enforce the compact.[47]

The language in the model legislation proposed here can also be modified, particularly if the goal is to short circuit specific types of adverse competition. For instance, job training programs could be excluded from the definition of subsidies as long as they are generally available and do not include language that discriminates against specific sorts of employment.

In any case, the purpose of this compact is to set up an agreement where all states benefit from the removal of the current destructive incentives to practice mercantilism. The outcome would essentially mimic the environment that would exist if the Commerce Clause was suitably interpreted to rule out present forms of discriminatory economic competition. In essence, it would recreate the truly free-market relationship between the states the Commerce Clause was intended to foster. Consistency in the language of the compact adopted by each state is key, however, as it would be in any treaty or other type of compact and should be settled at the outset before any state began to debate any version of the compact.

Conclusion

To date, attempts to overcome the temptation of policymakers to create or expand business subsidy programs has been spotty at best, even if there have been some short-term cessation of certain tax credits. Overall, however, the strategy of aiming at individual programs or tax credits has generally been an ineffective tool at overcoming the real collective action problem at the root of unhealthy, mercantilist competition between states that corporate welfare creates.

Only a universal approach is likely to solve this problem in an effective way. Only such an approach could create the environment in which healthy competition would predominate over the unhealthy forms of competition discussed in this study. With a new crop of governors and legislators coming into office in 2019 — many of whom are aware of the problems inherent in these sorts of unproductive subsidies — the time may be near when a number of states can compose a truly united front against select business subsidies by adopting a cease-fire treaty like the one outlined in this study.

Appendix: Corporate Welfare Prohibition Compact

The state of _________________ agrees to the following compact:

ARTICLE I

FINDINGS AND DECLARATION OF POLICY

- The party states understand that subsidizing some businesses at the expense of others is, over the long term, ineffective at best and harmful to the national economy and honest governance at worst.

- These policies are often enacted for the purpose of luring a company to relocate a headquarters or a part of a corporate operation to a state. Yet these actions often preclude a more healthy competition between states in which tax and regulatory barriers are lowered to benefit the general population and create a more favorable economic climate for all businesses.

- These policies also lead to an inefficient distribution of resources among the states, leading to increased costs and inhibiting the ability of the nation to compete internationally as well as domestically. They also contribute to corruption and the loss of faith in the basic fairness of our political and economic system.

- Therefore, the party states agree that their state government, or any political subdivision, shall not provide a subsidy to a private enterprise for the purpose of selectively supporting a specific industry or company, or to entice a specific industry or company to relocate a facility from one party state to another party state or open a new facility in a particular party state.

- The party states also agree that once enough states with representation sufficient to constitute a three-fifths majority in both Houses of the U.S. Congress become party states, the party states and their political subdivisions will cease and desist in providing any additional subsidies except to satisfy contractual obligations agreed to prior to the activation of this section.

ARTICLE II

DEFINITIONS

As used in this compact, unless the context clearly indicates otherwise:

- “Party state” means a state that has enacted a statute agreeing to this compact.

- “Political subdivision” means governmental branches, departments, agencies, counties, municipalities, special districts, as well as other governmental entities and quasi-governmental entities created by the authorization of law.

- A “subsidy” is an economic benefit, direct or indirect, granted by a state government or any political subdivision, including but not limited to direct grants, tax consideration, favorable bonding status, special district status, or any other benefit that has the effect of reducing governmental costs for a venture or class of ventures compared to others similarly situated, with the primary purpose or substantial effect of encouraging or maintaining within a state or political subdivision’s borders particular or specific classes of ventures in which private persons have a substantial financial or ownership interest. The economic benefits to private enterprise from the following shall not be considered a subsidy:

- Benefits from the government’s performance of essential government functions: specifically, benefits from: (a) The party state’s or political subdivision’s provision and maintenance of public infrastructure for general public benefit and for actual public use; (b) The party state’s or political subdivision’s performance of functions without which it would cease to exist as a governmental body; (c) The retention of private enterprise to perform functions of the type without which the party state or the political subdivision would cease to exist as a government body; and, (d) The procurement of supplies and services from private enterprise for the party state’s or political subdivision’s ordinary business operations.

- Benefits from lower taxes and less regulation; specifically, benefits from: (a) The general and uniform relaxation or repeal of regulations; (b) The general and uniform reduction or repeal of taxes, assessments or fees; (c) The relaxation or repeal of special regulations which, if not relaxed or repealed, would otherwise subject specific individuals, entities, or classes of individuals or entities to regulatory burdens in excess of those imposed generally and uniformly; and, (d) The reduction or repeal of special taxes, assessments, or fees which, if not reduced or repealed, would otherwise subject specific individuals, entities, or classes of individuals or entities to taxation, assessments, or fees in excess of those imposed generally and uniformly.

D. A “facility” includes, but is not limited to, a headquarters, warehouse, outlet, affiliate, or production facility of a company.

ARTICLE III

TERMS

Notwithstanding any state law to the contrary:

When the number of states sufficient to satisfy the conditions outlined in Article I, Section E, agree to the compact, the party state governments, or any political subdivision, shall not give a subsidy to a private enterprise for the purpose of selectively supporting a specific industry or company, or to entice a specific industry or company to relocate an existing facility from one party state to another party state or open a new facility.

ARTICLE IV

ENFORCEMENT

Notwithstanding any state law to the contrary:

- The chief law enforcement officer of each party state shall enforce this compact.

- A taxpaying resident of any party state has standing in the courts of any party state to require the chief law enforcement officer of any party state to enforce this compact.

ARTICLE V

COMPACT ADMINISTRATOR AND INTERCHANGE OF INFORMATION

- The governor of each party state or the governor’s designee is the compact administrator.

- The compact administrator of each party state shall maintain an accurate list of all party states.

- The compact administrator of each party state shall furnish to the compact administrator of each other party state any information or documents that are reasonably necessary to facilitate the administration of this compact.

- When the condition specified in Article I, Section E is satisfied, the compact administrator of each party state shall inform the party state’s congressional delegation, the president of the senate, and the speaker of the house and shall request that legislation that comports with Articles I, II, and IV of this compact be introduced and passed by Congress as soon as possible, and shall send copies of these communications to the compact administrator of each party state.

ARTICLE VI

ENTRY INTO EFFECT AND WITHDRAWAL

- This compact is effective when the conditions described in Article I, Section E are satisfied. Once the compact is effective, a state becomes a party to the compact and bound by its terms when it enacts a statute agreeing to the compact and written notice of such enactment is received by the governor of each other party state.