Critique of the Incentive Evaluation Commission’s Tax Incentive Evaluation Report: 2016

Author

Byron Schlomach

Abstract

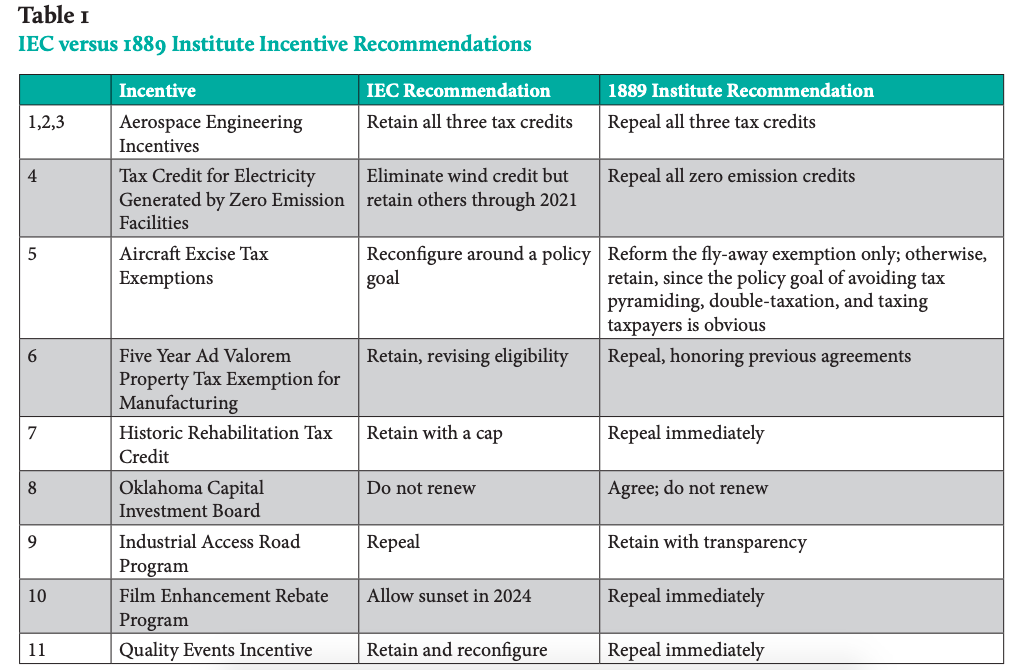

This paper looks at the first report of Oklahoma’s Incentive Evaluation Commission (IEC) and finds it wanting. The IEC was created to review Oklahoma’s many tax incentives for industry over a period of years. In their first round of recommendations, they suggest repealing only four of eleven reviewed incentives. The Institute suggests repealing nine. Apparently, the IEC is more interested in the status quo than real reform, having made unique recommendations with only $3 million in financial impact. Therefore, the IEC should be abolished.

Full Text HTML

Critique of the Incentive Evaluation Commission’s Tax Incentive Evaluation Report: 2016

Byron Schlomach

Abstract

Oklahoma’s Incentive Evaluation Commission (IEC) is a blue-ribbon panel assigned the task of reviewing the many business tax incentives and subsidies that litter the state’s tax codes. Based on the IEC’s work so far, there is reason to be disappointed. In its first completed round-robin review, it evaluates eleven programs and suggests retaining seven of them. The potential budget impact is a mere $3 million when the wind tax subsidy recommendation is excluded, since wind subsidies are already widely viewed as on the chopping block.

This report explains why nine of the programs, instead of only four, should be eliminated, for a total budget impact of $93 million with wind subsidies excluded. In addition to providing specific critiques of reviewed incentives, the paper explains why tax incentives and subsidies are bad policy in general.

The IEC appears likely to retain most incentive programs due to its flawed analytical methodology, as explained in the paper, so its impact on the state’s fiscal future will likely be negligible. In conclusion, the IEC should be repealed and disbanded.

Introduction

The Incentive Evaluation Commission (IEC) has submitted its first report with recommendations to the legislature on whether to retain or repeal the incentives that have so far been reviewed. This is a critique of that report, as well as a critique of the IEC review process in general.

The IEC was constituted in accordance with Title 62, sections 7002 – 7005, Oklahoma Statutes, passed into law in 2015. The law is fairly specific regarding issues that should be considered with respect to various business tax and subsidy incentives that the state offers. Oklahoma’s Office of Management and Enterprise Services provides support services for the IEC, has compiled a lengthy list of the incentives for review, and has provided expertise in the selection of outside consultants to aid the IEC in its duties.

The IEC’s report is quite lengthy, given the extensive descriptions of the history of each incentive as well as the issues surrounding it. This critique does not attempt to replicate or dispute the factual details of the IEC report, other than the results of economic modeling. Instead, it takes the IEC’s efforts at face value and merely attempts to add facts where possible, making separate and independent recommendations regarding each incentive.

In general, the IEC’s recommendations are found wanting and the IEC process is, so far, a lost opportunity. The IEC recommends retaining seven of the eleven incentives reviewed, albeit with some reforms, and for the most part, recommends no immediate action on those recommended for abolition, allowing them to expire according to sunset dates, sometimes years from now. They would end one transportation program, which does not impact taxes, right away. Their recommendations would yield $116 million to the state’s budget if they were realized immediately, but elimination of alternative energy tax subsidies is $113 million of this. Since alternative energy subsidies are generally considered to already be on the legislature’s chopping block, the IEC’s unique recommendations present a mere $3 million in value to the state budget.[1]

As Phil Gramm (economist, former Texas U.S. Senator) recently wrote in the Wall Street Journal, “The goal of tax reform is to collect revenues while reducing the distorting influence that taxes impose on economic efficiency and growth. The 1986 tax reform stripped out deductions and credits—which had distorted resource allocation and sapped economic efficiency—and collected roughly the same amount of taxes with a 28% top individual rate and a 34% corporate rate that had previously been collected with a 50% top individual rate and a 46% corporate rate.”[2]

The IEC could, and should, be the first step in a broader tax reform effort in Oklahoma that would mimic the 1986 federal income tax reform. Instead, the IEC seems bent on keeping the status quo. Meanwhile, only three states, Maryland, North Dakota, and Virginia, have more incentive programs than Oklahoma.[3]

This critique recommends repeal or allowing the short-order sunset of nine of the eleven incentives. The critique’s recommendations would yield $206 million in fiscal impact if they were realized immediately. Discounting alternative energy, the value of these recommendations amounts to $93 million, a full $90 million more than the IEC’s unique recommendations. Many of these recommendations directly contradict those of the IEC, as can be seen in Table 1.

A General Critique of Tax Incentives and Subsidies

For most economists, the holy grail of tax policy is to impose taxes in such a way that they minimize impacts on the economic choices people make as compared to the choices they would make if the taxes did not exist. Economists would ideally like to see tax systems that are as neutral as possible. That is, they would impact relative prices of goods and services very little compared to what relative prices would be if taxes did not exist. This allows economic decisions to be based on actual costs, as closely as possible, rather than costs made artificially low or high through government action.

Tax neutrality is important because an economy is most productive and affluent when economic decisions are made based on market-based prices, which best reflect the true costs and benefits of goods and services, especially inputs into production processes. For example, the federal government provides a politically popular mortgage interest deduction to the federal income tax. This artificially reduces the price of housing, which encourages larger and more numerous housing units than would occur without the deduction. Consequently, the United States sacrifices greater savings, greater business investment, and any number of other things that people could spend their money on in preference of mortgage payments. We are richer in housing that we otherwise would be, but poorer in other things, as well. The result is a distorted economy that is not as rich as it would be were the true costs of mortgage payments fully realized by individuals.

As two economists, who authored a New York state tax incentives study put it:

“Six widely accepted principles against which to judge tax policies are economic neutrality, equity, adequacy, simplicity, transparency, and competitiveness. An economically neutral tax does not influence economic behavior — individuals and businesses make decisions based on economic merit rather than tax implications. An equitable system treats similarly situated taxpayers similarly. An adequate tax system raises enough revenue to support desired government services and investments. A simple and transparent system is easy to understand, relatively inexpensive for taxpayers to comply with, and relatively inexpensive for the government to administer. A competitive tax system does not impede the ability of companies to compete with those located outside the state and does not limit the state’s ability to attract new business.

Almost by definition, business tax incentives violate these principles. Their explicit goal is to alter decisions, encouraging more of a particular activity in a state or a given area than private markets would undertake absent the incentives. Depending on the activity, this may be appropriate, but it places great responsibility on public officials to understand how the market is “wrong” and how the tax system can fix it. By lowering taxes for some taxpayers while keeping them higher for others, incentives may treat similarly situated taxpayers differently and can make it harder to raise adequate revenue with minimum public resistance. Finally, myriad eligibility rules and credit calculations violate the simplicity principle for taxpayers and tax collectors.”[4]

Many economists credit the 1986 income tax reform’s elimination of many deductions and credits (not including the mortgage interest deduction) with helping to produce and prolong the longest economic recovery in modern U.S history at the time. As Phil Gramm put it, “The economy boomed not only because the lower individual and corporate rates increased incentives to work, save and invest, but because stripping out tax-favored provisions reduced the drag on economic efficiency that is caused by allocating resources politically.” [5] (emphasis added)

Put simply, tax incentives and subsidies that often purposely distort economic decisions do not make us richer; they make us poorer. Tax incentives weight economic decisions in favor of politics rather than economics (true costs and benefits). Consequently, we lose. This has been illustrated in a unique way by economists that have looked at corporate activity in the districts of congressmen who gain leadership status. They found that corporate activity actually decreased once congressmen became more powerful, even though you would expect the opposite with these congressmen gaining even more benefits for their constituents. Politically connected corporations likely do well in these districts, but finding it difficult to compete, the unconnected flee or retrench, for a net loss to the district’s economy.[6]

Tax incentives and subsidies are simply redistributions from taxpayers in general to politically powerful constituencies. That power might come from numbers, as is the case with incentives and subsidies for sports venues and the fans involved, or from the popularity and wealth of the recipients, as is the case with film subsidies and sports venues, whose business owners are very wealthy. Regardless, there is little to no evidence that incentives, on net, improve the economic vitality of states and other governmental jurisdictions that hand them out. They doubtlessly do improve the bottom lines of those who directly claim the incentives, but this comes at the expense of the economic health and vitality of not only state and local taxpayers, but of the nation as a whole.

Tax incentives and subsidies doled out by states and intended for specific industries and companies fundamentally violate one of the reasons that the U.S. Constitution was created. During the Revolution and before the Constitution was adopted, states were free to erect trade barriers, mainly tariffs, against each other, artificially favoring themselves over other states through direct means. By taxing the production of specific industries’ production in a different state, industries located within the taxing state gained advantage, at least as long as other states did not retaliate with tariffs of their own.[7] Trade suffered, comparative advantages and specialization were less likely to be harnessed, and the economy of the former colonies as a whole suffered greatly. Among other issues, the U.S. Constitution was written to grant the national government sole power to regulate interstate trade, and Congress almost immediately abrogated state tariff policies upon the Constitution’s ratification.

Interstate tariffs – taxes imposed by one state against the economic activity of another state – rendered illegal with passage of the U.S. Constitution, can be thought of as one side of a coin. On the other side are tax incentives and subsidies – tax benefits and grants from one state to prevent movement of economic activity to another state. Because tax incentives and subsidies calculated to benefit the doling state over other states can be more difficult to define and identify as such, and because some tax deductions, credits, and exemptions are economically justifiable, making these artificial advantages illegal is difficult. But, Congress could and should act under the Constitution to make them so.

Another problem with tax incentives and subsides is that many of these programs inevitably favor large businesses and businesses that have made a practice of being politically connected. Some programs focus on companies that provide health benefits and above-average wages. This clearly favors long-established big business over startups. Such requirements favor big businesses that enjoy significant economies of scale and can afford the additional personnel needed to administer incentive-required employee benefits, in addition to the cost of the actual employee benefits. Some businesses, especially big businesses, are favored over others, especially small businesses, even though they are competing with each other. Government picking winners and losers not only violates sound economic principles but also offends basic notions of fairness and justice. This brings into question whether the purpose of business incentives is to produce economic growth or if it is to allow the politicians and bureaucrats who administer the programs to rub shoulders with the rich and powerful.

Tax incentives and subsidies like the aerospace engineer incentives and the 5-year ad valorem exemption, increase the cost of living in the state by favoring those with relatively high incomes. One advantage Oklahoma has over all but a handful of states is our relatively low cost of living. This helps to keep wages in the state relatively low and competitive, which we need to do given the state’s geographic location and the policies of the states around us. Purposely subsidizing imported high-income labor seems like a good way to increase overall state incomes and reduce demand on state-provided services. However, since there is no evidence the businesses that employ high-income labor are actually being attracted by incentives, the incentives cause low-income taxpayers to subsidize high-income lifestyles. High-income individuals, in turn, bid up the cost of land and housing, and potentially everything else those with modest incomes also purchase.

Again, even though states and local governments dole out incentives in the form of credits, subsidies, deductions and exemptions specifically to impact business location decisions supposedly in competition with other state and local governments, there is no evidence that they succeed. As noted in numerous studies, the authors of the New York state incentive study point out that “there is no conclusive evidence from research studies conducted since the mid-1950s to show that business tax incentives create net economic gains to the states above and beyond what would have been attained in the absence of the incentives. Nor is there conclusive evidence from the research that state and local taxes, in general, have an impact on business location and expansion decisions.”[8]

Ultimately, besides distorting economic activity to the point of shrinking it, and favoring privileged constituencies, tax incentives and subsidies accomplish nothing except to distract and detract from the business of sound governance. Instead of managing excellent road, sewer, water, and justice systems, government officials pursue meet-and-greets with the rich and powerful while telling themselves they’re doing the work of the people.

The Incentive Evaluation Commission’s Process

Although the IEC has attempted to be open in its deliberations and proceedings, there is room for improvement. Much of the process has been driven by the staff of the Office of Management and Enterprise Services (OMES). This is to be expected, given the nature of a blue-ribbon panel, and the members of the IEC have clearly been welcome to exercise their legal and proper influence and have done so. Public input has been fairly limited up the time of this writing, perhaps necessitated at least partly by the contracted length of time the IEC had to get its work done in its first, start-up year of evaluations.

Solicited public input has been limited and has mostly been in favor of incentives. In one early meeting, the IEC heard some invited, specific testimony from two individuals on ways to structure business incentives. These were the director of the Oklahoma Policy Institute and a gentleman with 30 years of experience in Mississippi’s economic development efforts who was brought here by Oklahoma’s Chamber of Commerce. Testimony from the former mostly consisted of the “right” way to do economic incentives, acknowledging they can be done improperly and are sometimes simply corporate welfare. Testimony from the latter extolled the virtues of government involvement in economic development, but also stressed there are “right” and “wrong” ways to provide for incentives. There is nothing in the last 30 years of Mississippi’s macro-economic history that indicates reasons that its economic development efforts should be replicated in other states.[9]

Little testimony hostile to incentives in general was taken, and appears never to have been sought, although there are many reasons to question the legitimacy, productivity, and philosophy behind incentives.[10] In fact, there is a rich academic and think-tank literature highly critical of incentives and subsidies at all levels of government. No doubt, several organizations and individuals would have provided testimony to the effect that tax incentives and subsidies are inherently flawed and should be repealed. A number of progressive, conservative, and libertarian organizations could have been called upon to provide such a perspective.

Perhaps one reason nothing openly hostile to incentives in general has been heard by the IEC is because the IEC’s chairman is personally involved in economic development efforts that often employ incentives. Lyle Roggow is president of the Duncan Area Economic Development Foundation, a sales-tax-supported non-profit, quasi-governmental organization. This brazen conflict of interest is a product of the law creating the IEC which specifically requires that the president of the Oklahoma Professional Economic Development Council or his designee be a voting member of the IEC. Mr. Roggow is the designee. Such a member should be appointed in an ex officio, advisory capacity, rather than as a voting member with the realized potential to chair the commission, which appears to make a mockery of the entire process.

While the use of consultants does not, in itself, present an obvious problem, and is even necessary given the blue-ribbon nature of the IEC, on hindsight, there are incentive issues that make it difficult for consultants to be completely objective. PFM Group consults with all types of state and local governmental entities. These include school districts, higher education, hospital systems, municipalities, utilities, and transportation systems, among others. Two of PFM’s listed clients are Oklahoma City and Will Rogers International Airport.[11]

Very often, leaders of governmental organizations weigh in positively on economic development efforts and incentives or even negotiate incentives themselves. For example, Tax Increment Finance (TIF) districts should be included on the list of incentives to be reviewed, although they presently are not.[12] Oklahoma City is a serial implementer of TIF districts and PFM’s objectivity would clearly be suspect if it were reviewing that particular incentive. But there are other incentives up for review that Oklahoma City might have something to say about. The aerospace engineer incentives, for example, benefit an industry that impacts the Oklahoma City metro. It would be very unusual for an organization that has likely consulted with clients who want to justify such incentives to be completely objective in an evaluation of such incentives. How many such clients would PFM gain in the future if PFM made a practice of recommending against incentives?

Issues to Consider in Evaluating Incentives

A Note on Fairness

Economic analysis does not generally speak to fairness for the simple reason that it can be a slippery slope and there is not a widely agreed definition of fairness. However, tax and spending policies almost beg for a fairness discussion because government and, therefore, coercion are involved. Thus, fairness should be part of the conversation and part of the Commission’s considerations.

Many of the incentives the Commission has reviewed and will be reviewing in the future effectively rob from the poor and middle class and give to the rich with the vague promise that in some way the money will trickle back to those forced to cough it up in the first place. Not only is this faulty economic reasoning, it is a gross injustice. On this basis alone, most incentives should be ended.

While a tax credit creates an appearance that only one’s own money is at stake, credits are a discretionary exercise on the part of government and they impact the tax burden borne by others. Some tax credits are arguably justified, but tax credits that are for anything other than paying individual taxpayers back for initially funding public assets or for making the tax system as economically neutral as possible simply distort who ultimately pays the taxes and economic decision making.

A Note on Economic Modeling

Since the comments on the specific incentives reviewed by the IEC below are not based on modeling, and since modeling carries an air of certainty, the following critique of modeling argues that such confidence in economic modeling is not justified.

Economic modeling like that relied on by the IEC’s consultants is a highly inexact “science” often as akin to fortune telling as predicting or reflecting reality. A commonly-used model initially developed by the Forest Service called IMPLAN (Impact Analysis for Planning) is the one employed by PFM. IMPLAN is fairly well-known and understood although it is now produced by a purely commercial venture. This author is more familiar with REMI (Regional Economic Models, Inc.), a similarly-constructed model, and STAMP (State Tax Analysis Modeling Program), which is somewhat different in its underlying assumptions, but economic models share some basic similarities.

Economic models are quite complex. Even when the basic equations are revealed, few model users understand them. What’s more, the models just mentioned are custom-built for various regions using equations derived from a series of assumptions. Models are assembled using mathematical relationships that have been estimated at various times over the years and reported in economic journals and other sources. When this is done, basic production and consumption behaviors reflected in the equations are assumed to be the same for every region modeled. This faulty assumption rears its head when a model for a region is being constructed and its results are compared to actual data (to the extent that such data can be obtained; much regional data is extrapolated and unconfirmed). Each regional model must be adjusted to “solve.” That is, equation parameters are altered slightly in order to make them all work together and produce outputs consistent with real-world data. To sum up, errors and erroneous assumptions are stacked one on top of another in constructing economic models.

IMPLAN and REMI have multipliers built into them which reflect the reasonable belief that money spent is often re-spent, and then spent again, so as to produce more economic activity than an initial expenditure would seem to justify. So, $10 million in new investment, which flows to workers and businesses, is spent by the workers and businesses in other areas in a community so that the $10 million produces perhaps as much as $30 million in total economic activity. But, this multiplier effect assumes that the initial $10 million dropped like manna from heaven, because if it were taken from the pockets of others in the community, the new investment’s impact would be offset by reduced spending by those others. It is left to the users of models like IMPLAN and REMI to have the sophistication to offset new spending appropriately when the spending is financed within a region. Often, model users fail to account for where the money comes from, and this is a difficult task anyway, since doing it right would require the modeler to figure out the many snippets of funds that would come from various sectors of the economy – an impossible task.

In addition, model users often do not reveal their inputs into a model, which can determine the outputs regardless of a model’s perceived accuracy. Thus, all economic modeling tends to have a “black box” component. Most of the time, there is no way to confirm with certainty the economic claims being made for a policy because we cannot compel a model user to reveal their inputs. Consequently, good economic common sense trumps highly sophisticated mathematical modeling in one’s ability to understand the effects of economic policies.

Sometimes, model users are hesitant to reveal their inputs because they would look strange. Models often result in unreasonable outputs that can only be corrected with unreasonable inputs. For instance, economic models generally employ a production equation that follows a particular functional form.[13] The production function views labor and productive capital (machinery and buildings) as substitutes, with labor and capital seamlessly replacing each other in the production process. So, if a property tax is reduced and a sales tax is increased to balance the change, this greatly increases the price of labor compared to capital and a model will generally return results that indicate dramatically increased unemployment. Yet, if this were true, our current economy should be characterized by widespread unemployment since we have more productive capital than ever.

The IEC collectively made the decision to follow their consultants’ recommendation that only primary economic effects would be modeled. Primary effects are reactions to a policy change by economic actors immediately impacted by the change. For example, a federal tax imposed on luxuries such as furs, private planes, and yachts during the George H.W. Bush administration had the primary effect of raising the overall price of these items and driving sales down, as would be expected by the law of demand. Part of the primary impact was a loss of jobs in these industries. Secondary impacts included the loss of income in other industries that served the workers in these industries who no longer had jobs and the overall negative impact on the communities in which they lived. Such secondary effects can be quite profound. There is a further loss of investment and, once targeted, industries are slow to recover even after the target is removed for fear of being targeted again.

Even primary effects are not truly known, however. Presumptions have been made in the IEC analyses, for example, that aerospace engineers would not have been hired but for the incentives, that some historical preservation has only occurred due to an incentive, and that historical preservation has an economic benefit. None of these are actually known. In fact, company location incentives that are often employed by states usually amount to little more than a rounding error in the accounting of the large corporations these incentives often target. It is difficult to believe fundamental business decisions are significantly impacted by incentives under such circumstances, yet that is the presumption made by the IEC’s consultants.

Additionally, tax breaks for some can signal others that their economic efforts are not wanted. Studies have shown that some tax privileges actually result in lower economic growth overall due to the negative effects of crony policies. As noted above, these policies present greater risk to those who doubt whether they can gain from them while their competitors do so. Consequently, they avoid places that practice subsidies for fear of competitors being favored. Thus, the multipliers so often used in modeling that turn $10 million expenditures into $30 million in economic activity are largely meaningless, even when modelers do a good job of accounting for sources of funds. It is literally impossible to anticipate the kind of discouragement of economic activity described here and include it in a modeled analysis. Models’ multiplier claims are also impossible to accurately empirically verify because the future is uncertain and economic shocks and their impacts cannot possibly be fully taken into account so that a subsidy’s or incentive’s exact impact is isolated for measurement. The only way to evaluate the impacts of incentives is to do so statistically and in general, and the results of such analyses confirm these programs’ ineffectiveness.

Even where primary effects are obvious, as with wind generation subsidies, there is a problem with mistaking what we can easily see as the actual and full effects while there is much that is unseen. Unseen is the diversion of talent and human energy from other endeavors people are willing to pay for voluntarily. Unseen is the negative impact on other industries that rely on the same materials as wind generation and must compete with a subsidized industry for those resources. Unseen is the future when subsidies end and the infrastructure to support windmills becomes obsolete and abandoned. Unseen is what taxpayers would have invested in, and spent their money on, had government not confiscated their funds through taxation.

To make these remarks more concrete, here is an example. Were modern economic models applied prospectively to the exemption of employer-paid health insurance from income taxation and payroll taxes, there might have been some prediction that health insurance prices would rise. However, the development over time of high-cost health care such as the extinction of hospital wards and the over-use of technology could not have been anticipated by any model. Models fail to take account of the waste inherent in businesses actively seeking favor from government and the amount of talent and effort diverted to do so. Models do not and cannot fully account for the negative effects from diverting resources toward industries whose size or very existence depend on government incentives instead of market forces.

Aerospace Engineering Incentives

Commission Recommendation: Retain all three Aerospace Engineering tax credits.

1889 Institute Recommendation: Repeal all three Aerospace Engineering credits.

Comments here apply to three separate tax credits for aerospace employers and employees. The aerospace tax credits are for:

- Tuition Reimbursement by Aerospace Employers

- Compensation Paid by Aerospace Employers

- Aerospace Engineer Employees

The first two credits go to companies that hire aerospace engineers. Employers can claim a credit for reimbursing newly-graduated engineers for up to 50 percent of their college tuition. For up to five years, employers can claim a credit of 10 percent of an engineer’s salary. The last listed credit can be claimed by individual engineers. They can claim up to $5,000 per year for five years, a significant boost to take-home income.

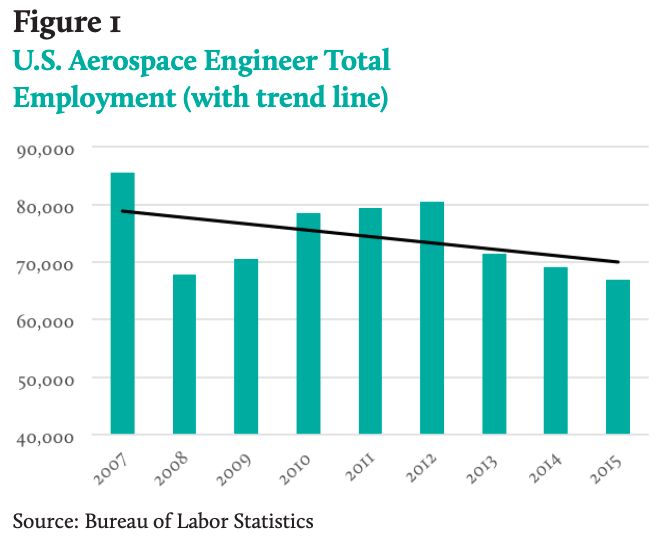

Although there is no way to know for certain, national aerospace engineer employment data suggest that Oklahoma’s tax credits are needless and have had no employment impact whatsoever. Oklahoma’s aerospace engineering employment growth after 2008, highlighted in the commission’s analysis and credited to the tax incentives, would have likely occurred without the incentives due to reduced employment of aerospace engineers across the nation, which increased availability of engineers, at the time the incentives were adopted. In 2007, 85,000 individuals were employed as aerospace engineers across the nation. In 2009, only 70,000 individuals were so employed. The recession and national defense policy changes eliminated many aerospace engineers’ jobs. To the extent that aerospace employers in Oklahoma needed engineers, they were arguably readily available by 2009, regardless of tax credits, since engineers were simply more available in general. As of 2015, only 67,000 individuals were employed as aerospace engineers in the U.S. [14]

Many industries complain of labor shortages, so why subsidize the aerospace industry versus any other? Another question is, why should the state effectively subsidize professionals with relatively high incomes? The answer is that the aerospace industry in Oklahoma is being specifically targeted for favorable treatment and expansion/retention. More particularly, a limited number of employees and a very limited number of employers in a highly limited geographic area are being targeted to benefit from these incentives. But, this type of selective benefit tends to retard economic activity that might otherwise occur in other industries that would arise and grow more organically with more lasting effects without distorting the economy overall.

The economic impact estimated by the Commission’s consultants effectively assumes that all the jobs for which credits have been forthcoming would not have occurred without the credits. This is an erroneous assumption. The analysis also fails to consider the impact of economic “crowding out” when other industries are negatively impacted by a favored industry’s increased demand for resources relative to what it would have been without the special tax privilege.

Tax Credit for Electricity Generated by Zero Emission Facilities

Commission Recommendation: Eliminate the wind energy credit by January 2018 but retain the credit for other forms of renewables through 2021, capping total credits.

1889 Institute Recommendation: Repeal all zero emission credits with immediate effect, grandfathering only those projects already completed or under construction.

The IEC consultants’ report acknowledges that Oklahoma has significantly surpassed its renewable power generation goals. Therefore, there is no reason to continue the program for additional facilities through 2021 based on this fact alone. What’s more, renewable energy subsidies at the federal level, started in no small part in an effort to gain greater national energy independence, have been rendered moot by technological changes in fossil fuel production that have come much closer to achieving this goal.

Renewables continue to be generously tax subsidized by the federal government due to highly disputed claims regarding global warming and carbon dioxide emissions. While parts of sparsely-populated Oklahoma benefit from increased employment from wind energy, spending on wind energy represents economic waste due to the need to replicate wind’s unreliable generation capacity with traditional generation. Subsidizing wind generation is like repeatedly having a sidewalk poured, torn up, and re-poured in the middle of a desert for the sake of providing jobs to a few families who live there.

The IEC’s consultants make it seem that wind generation is part of the reason for Oklahoma’s relatively low electricity rates. However, wind energy actually leads to increased electricity rates due to wind’s intermittency and the need to replicate wind generation capacity with traditionally-powered generators. The economic modeling in the IEC’s report fails to take these considerations into account.[15]

A separate problem with wind has to do with voltage variations due to changes in wind speed. Technology has helped to alleviate voltage dips and spikes due to wind variability to some degree, but not completely. Despite the amount of wind in Oklahoma, there are also windless days, as occurred in Germany in recent years when their reliance on wind generation crippled the economy. Due to backup generation installed privately, Germany’s carbon dioxide emissions are higher than ever.[16]

The IEC report is misleading when it compares wind’s cost of generation only to that of natural gas. When it comes to reliable sources of electricity, traditional generation is really the only option outside of a huge investment in excess wind capacity in the hopes that while some windmills are becalmed, the wind will be blowing elsewhere. Were renewable sources reliable enough that they could be relied on to produce constant voltage on the state’s grid at a reasonable cost, renewable sources of energy would have been adopted without tax incentives. The very fact that tax incentives are necessary testifies to the fact that renewable energy sources are, on net, more costly. Thus, claimed economic benefits from subsidizing renewable energy are simply spurious.

Aircraft Excise Tax Exemptions

Commission Recommendation: Reconfigure by focusing the exemptions around a policy goal.

1889 Institute Recommendation: Reform the fly-away exemption to include all sales of aircraft to out-of-state owners who store their aircraft in their state of residence, but retain other exemptions since the policy goals of avoiding tax pyramiding, double-taxation, and taxation of taxpayers are obviously not in any way intended as incentive programs, but are part of an economically sound tax policy.

The aircraft excise tax is a separate aircraft sales tax. Sales taxes always have exemptions associated with them designed to avoid tax pyramiding, to ensure tax equity, and to avoid taxation between different levels of government. Pyramiding occurs when a tax builds upon itself. For example, if iron ore were sales taxed, the tax would be built into the price charged by steel manufacturers since the steel price would be calculated on actual cost of steel production plus the tax. In turn, the tax on a car would be calculated the cost of steel, including the tax, which means a sales tax on a car would be partly calculated on the amount of tax charged on inputs. Thus, the tax builds on itself to become a large and hidden share of the cost of producing a car, which distorts the public’s buying decisions as well as business decisions by, for example, incentivizing businesses to vertically integrate only to avoid taxes rather than for truly economic reasons.

Four of the 18 exemptions listed by the IEC simply avoid pyramiding. For example, aircraft used for agricultural spraying and for use by commercial airlines initially appear to make little sense given that there is no exemption for other aircraft that are used as an input in business. However, agricultural spraying aircraft are highly specialized and are almost never used for anything other than agricultural spraying. That is, they are pure inputs. The same is true for commercial aircraft. Thus, these exemptions are, in fact, for the purpose of avoiding pyramiding and are therefore completely justified. Other types of “business” aircraft can and often are used for personal purposes. Were there a way to ensure other aircraft were pure inputs, then it would be different, but tax equity would seem to dictate that an executive using a jet for personal purposes should suffer the same tax as a hobbyist in a small plane.

Most of the other exemptions such as if an aircraft is transferred to a corporation for organization purposes and business to business transfers for corporate reorganization or when a dealer purchases aircraft for resale, simply avoid double taxation, and are numerous given the many ways aircraft ownership is formally transferred on paper, but not in actuality, as with corporate mergers. Remaining exemptions are for other levels of government, such as when the federal or state government make aircraft purchases, a long-standing practice of not requiring taxpayers to pay themselves at different federal and jurisdictional levels.

Consideration of these exemptions should have been disposed of without any need for modeling or highly detailed review. Given standard practice in the construction of sales taxes, the policy goals of these exemptions should have been obvious and there is no need to state them in law. The one exemption for aircraft over $2.5 million and flown elsewhere is an outlier, with no economic rationale for exempting only very expensive aircraft. That exemption should be extended to all aircraft, regardless of value, since a state’s sales tax should, in principle, only be paid by the state’s residents, so as not to disadvantage Oklahoma producers.

Five Year Ad Valorem Property Tax Exemption for Manufacturing

Commission Recommendation: Retain but consider revising program eligibility requirements.

1889 Institute Recommendation: Repeal immediately while honoring agreements already made.

This exemption is highly distorting. One reason for tax equity is economic. By treating all economic activity the same as much as possible, resources are free to flow most closely to what a true market ideal would dictate. This is desirable because actual (not artificial) costs are fully taken into account in making economic decisions, including investment decisions. This makes it possible for true costs to be weighed with benefits reflected in people’s willingness to pay that cost as transmitted through prices.

Tax credits and exemptions generally distort relative costs and prices even more than if taxes were fully applied to everyone equally. Consequently, over-investment occurs in some industries while under-investment occurs in others, all of which could be avoided if taxes were applied equally.

Additionally, this exemption distorts decisions being made by government. County tax assessors decide to grant this incentive costlessly since the state makes up for the losses. So, if a community like Lawton were to ask the Comanche County assessor to approve an application by a Lawton manufacturer for an exemption, there is no incentive for the assessor to say no, even if the assessor knew the manufacturer would have located in Lawton, regardless of the exemption. This makes the program ripe for abuse from an economic point of view, and possibly from a legal one, given that the program does not appear to have effective oversight. And, while counties that grant this exemption do so costlessly, the rest of the state pays the costs. Thus, purchased economic benefits that might occur in Lawton are partially paid for in Stillwater. This is because the state makes the county financially whole, and state taxes, paid across the state, are potentially higher than they otherwise would be, or state-financed programs that benefit the state are smaller than they otherwise would be.

Programs like this one especially seem to inevitably favor large businesses and businesses that have made a practice of being politically connected. The focus on jobs that provide health benefits and above-average wages clearly favors long-established big business over startups. The structure of this incentive favors businesses that enjoy significant economies of scale and can afford the additional personnel needed to administer such programs in addition to the cost of employment benefits. Big businesses are especially favored over small businesses, even though they are competing with each other. Government picking winners and losers not only violates sound economic principles but also offends basic notions of fairness and justice.

Finally, the economic modeling used to justify retaining this program assumes that all investments made that claim this subsidy were only made because of the subsidy. This is faulty analysis. The analysis also cannot possibly account for the investments not made as a result of some investments being subsidized.

Historic Rehabilitation Tax Credit

Commission Recommendation: Retain but adopt an annual cap.

1889 Institute Recommendation: Repeal immediately.

The IEC report notes that the growth of states’ historic preservation incentives is at least partly driven by a desire to leverage the Federal Historic Preservation Tax Credit which is a far bigger driver of behavior than the state’s credit, which is much more modest.[17] Oklahoma’s state credit explicitly piggybacks on the federal credit, which applies to income-producing buildings. These are not necessarily open to the public, so their historic value for the community is largely derived from exterior aesthetics. While major, well-known buildings with large publicly-accessible interior spaces would seem to justify a program like this one, the fact is that these characteristics are not required for a building owner to enjoy the benefits of the program. The preservation of old warehouses for the sake of only their exterior walls, driven in part by a tax credit like this one is indicative of a program run amok.

Such differential tax treatments distort economic decisions (in this case, whether to rehabilitate historic properties) by artificially altering the apparent costs of those decisions. This is why tax policy should be as neutral and equitable as possible, so that post-tax decisions are as nearly the same as they would be if taxes did not exist. Clearly, this tax credit is intended to distort decisions in favor of rehabilitating historic properties. There is no clear economic or social justification for this policy, however. There is no way to evaluate whether the distortions caused by the credit are worthwhile to the general public.

Suppose a small government, in order to achieve its goals, must have $1 million in revenue. If it grants tax credits in the amount of $10,000 to a particular constituency, like people who own historic structures, all the other taxpayers must make up for the revenue loss. Yet, all other taxpayers do not benefit from the historic property. Many may not care at all about that property. In addition, the artificially lower cost of rehabilitation keeps what is likely a high-cost structure in place when a newer structure with lower costs of operation would have been built elsewhere. In other words, such distorted decisions result in a less efficient (more costly) economy and unevenly-distributed government benefits.

Oklahoma Capital Investment Board (OCIB)

Commission Recommendation: Allow OCIB to sunset on its current sunset date, June 30, 2018, which allows time for wrapping up current operations.

1889 Institute Recommendation: Follow the IEC’s recommendation.

The consultants (and IEC) are perfectly correct to recommend that this program be allowed to sunset, giving time for OCIB to wrap up its operations and obligations. The only rationale for this program is that a government-constituted body of civic-minded individuals would recognize market opportunities otherwise unrecognized by banks, venture capitalists and other investors who make it their business to seek out profit opportunities, wherever they may be. OCIB’s creation seems to reflect a presumption that venture capitalists had developed some sort of animus against Oklahoma. However, to the extent that OCIB was created to seed a venture capital industry in Oklahoma, it can be said that it succeeded and should be disbanded. To the extent that a venture capital industry might have developed on its own, OCIB is a failure, and should be disbanded. Either way, it is time for OCIB to end. The IEC and its consultants are correct to view OCIB’s claims of considerable positive economic impacts with a critical eye. No evidence is presented by OCIB or its economic consultants that the loans and investments OCIB has provided would not have occurred in the private sector anyway.

Industrial Access Road Program

Commission Recommendation: Repeal.

1889 Institute Recommendation: Retain, but make the decision-making process transparent and exercise oversight.

It should be noted that this program is unlike the others reviewed by the IEC. It is not a tax credit or deduction. Tax credits and deductions involve costs that, while estimates of these are available, the legislature often fails to acknowledge. This program involves an explicit appropriation whose costs, by virtue of its being an appropriation, are explicitly recognized by the legislature. What’s more, it is not clear that this program is an “incentive” at all. Government incentives usually take the form of tax benefits or explicit subsidies that are internalized, becoming private assets for those incentivized. It is not clear that the access roads provided under this program become private assets (though it is also not clear that they do not).

Road agencies must be nimble enough to react to unexpected significant needs. Road placement should not be what determines economic need and development, but just the opposite. Roads should accommodate transportation needs as determined by private investment decisions. This program appears designed to do the latter, which is proper.

Substantially due to the participation of the Federal Highway Administration in funding roads, state highway departments program road funding according to multi-year plans that go through layers of approval and are difficult to change. This makes it difficult to respond to needs on the sort of time-tables under which private enterprise operates. For obvious reasons, new industrial facilities tend to locate near major transportation corridors, but due to noise and other environmental concerns, they might have good reason to locate where connector roads are not well-developed or are non-existent. If these roads allow access to other properties (i.e., are not private drives), they are legitimate public investments. A highway department should be able to respond to such needs in a timely manner. Thus, the need for programs like the Industrial Access Road Program.

The best way to evaluate this program would be to review decision-making processes to make sure they are being made fairly and without prejudice, but only on the basis of true need. The IEC’s consultants are entirely justified in criticizing the lack of information on how decisions are made in determining how this program’s yearly-average $2.5 million appropriations have been or will be spent. They are also justifiably critical of the lack of data about the economic benefits of the specific road projects funded through this program. These data should be readily available to the legislature and it is a shame that they have not been long demanded by the legislature.

Film Enhancement Rebate Program

Commission Recommendation: Allow to sunset in 2024.

1889 Institute Recommendation: Repeal immediately.

This sentence from the IEC report on the Film Enhancement Rebate Program could be applied to most of the tax credit incentives reviewed by the IEC so far, “Regardless of how efficiently film incentives are administered, the return on investment to the state will likely always be negative.”[18] Given the typically generous nature of the analysis applied to other reviewed incentives, the legislature should stand up and take notice of such a negative remark. With respect to film incentives, it is arguable they have the most temporary impact of any of the incentives even though they simultaneously arguably have the very effect they claim, which is to attract film-making activity to the state.

Most states provide some kind of film tax incentive. Oklahoma’s incentive is relatively modest.[19] This benefits Oklahomans because the modest nature of Oklahoma’s film incentive has limited the state’s exposure to what amounts to an economic rip-off. While there is evidence the film production incentives in other states have attracted production from California, there is no evidence that this has led to lasting industrial migration from California. In fact, there has been a trend to reduce film incentives in other states for this very reason.[20]

While not every filmmaker strikes it rich, tax incentives for an industry as successful as the American film industry seem particularly unjust when taxpayers, who are customers of the industry and buy film tickets that already make filmmakers wealthy, are forced, in turn, to subsidize that industry. Industry clusters arise spontaneously due to a confluence of factors and it is a mistake for government to attempt to replicate clusters in competition with other governments. This is why tax incentives are generally an exercise in futility.

Quality Events Incentive

Commission Recommendation: Retain and reconfigure to make it easier to apply for grants under this program.

1889 Institute Recommendation: Repeal immediately.

It’s a very simple question. Why should dollars collected from Altus be used to promote/support an event in Broken Arrow? The statewide economic spillover effects of events held in any particular part of the state are extremely limited. For some whose taxes are used to promote an event, there is nothing but a negative return. The fundamental question here is why the state should be involved in this sort of funding in any way, shape, or form.

There is no traditional role here for state government. A road project in Broken Arrow does not directly benefit Altus, except that this is a traditional state role, and Altus has a chance to have its road needs met as well. Event funding is different in that some communities do not necessarily even want events to occur there, yet they are forced through this program to support events elsewhere, from which they do not profit in any way. Further, unlike roads that most people drive on, most people in a community do not attend, or in any way participate, in these events, and might even be inconvenienced by them.

This incentive is not only unfair and immoral in its impact, but it is, at best, economically flat. Economists have investigated claims regarding the economic benefits of various entertainment venues that are subsidized in some way and find those claims wanting. The economic impacts are localized and are often scavenged from other areas. The only exceptions are when outside tourism is greatly enhanced, but even this has resulted in a type of trade war among states. The small size of this program makes it clear that it is not attracting significant activity from out-of-state.

Conclusion

Although this first round of incentive evaluations by the IEC is a relatively small sample, the results of the IEC’s efforts thus far do not bode well for the future. Oklahoma’s economy needs greater diversification, and the state has attempted to bring this about partly through tax incentives that are being reviewed by the IEC, but there is no hard evidence these programs have worked. Many of these programs impact the state’s income tax, whose rates have been brought down in recent years, making many incentive programs even less likely to have an impact in the future than they have had in the past.

While the IEC’s consultants have performed good work in bringing together factual information about incentives, the overall value of the IEC is highly questionable. The use of economic modeling, which adds significantly to the cost of the IEC’s work product, is of little real value in evaluating whether to keep an incentive in place. What’s more, if the IEC had followed principles for evaluating tax policies consistent with limited government, the obvious answer to the question of whether to keep most incentives would be a simple no. An expensive and time-consuming process is simply not necessary if there is no effort to paper over the ineffectualness, unfairness, and negative impacts of tax incentive and subsidy programs.

Instead, it is clear that the IEC is most likely to recommend that the state retain the lion’s share of incentives. This, in turn, means that the IEC is unlikely to make a significant dent, one way or another, on Oklahoma’s fiscal future.[21] With this being the likely case, the obvious question to be asked at this point is, “What’s the use of the IEC, given that the benefits of its work are likely so limited?”

So, in addition to the recommendations summarized in Table 1 of the Introduction, one last recommendation is added here. Save any added expense and trouble of the IEC, and repeal it now.

_________________________

- Incentive Evaluation Commission, Tax Incentive Evaluation Report 2016 (Oklahoma City, OK: State of Oklahoma, 2016), http://iec.ok.gov/sites/g/files/gmc216/f/Tax%20Incentive%20Evaluation%20Report%202016.pdf. ↑

- Gramm, Phil, “How ‘Border Adjustment’ Poisons Tax Reform,” Wall Street Journal, February 22, 2017, https://www.wsj.com/articles/how-border-adjustment-poisons-tax-reform-1487807100. ↑

- “State Business Incentives Database,” website, Council for Community and Economic Research (C2ER), http://www.stateincentives.org/. ↑

- Rubin, Marilyn M. and Donald J. Boyd, New York State Business Tax Credits: Analysis and Evaluation (Albany, NY: New York State Tax Reform and Fairness Commission, November 2013), 1 – 2, www.politico.com/states/sites/default/files/131115__Incentive_Study_Final_0.pdf. ↑

- Gramm, “How ‘Border Adjustment’ Poisons Tax Reform.” ↑

- Cohen, Lauren, Do Powerful Politicians Cause Corporate Downsizing? working paper, October 7, 2011, http://www.laurenhcohen.com/assets/envaloy.pdf. ↑

- Bane, Frank, “Interstate Trade Barriers: General Introduction,” Indiana Law Journal, December, 1940, http://www.repository.law.indiana.edu/cgi/viewcontent.cgi?article=4318&context=ilj. ↑

- Rubin and Boyd, New York State Business Tax Credits, 11. ↑

- The IEC had previously heard from a representative of the Pew Charitable Trusts who talked in general about other states’ efforts to review their incentives. See “Amended Minutes, Special Meeting, Incentive Evaluation Commission, April 19, 2016,” at http://iec.ok.gov/sites/g/files/gmc216/f/IEC_2016-04-19_%20Amended%20Minutes.pdf. ↑

- Testimony from the general public was taken on November 10, 2016. Those testifying were expected to address only specific incentives and IEC recommendations. See “Special Meeting Minutes, Incentive Evaluation Commission, Nov. 10, 2016,” at http://iec.ok.gov/sites/g/files/gmc216/f/IECMinutes11102016_0.pdf. ↑

- “Selected Client List,” website, pfm.com, https://www.pfm.com/clients/client-list/. ↑

- TIFs have an impact on school finances, and by extension, state finances. See Byron Schlomach, Tax Increment Finance and Suggestions for Reform (Oklahoma City, OK: 1889 Institute, August 2016), http://nebula.wsimg.com/0dcfc8fd9a848b5a4d8d3d4f5301ed8f?AccessKeyId=CB55D82B5028ABD8BF94&disposition=0&alloworigin=1. ↑

- The functional form most commonly used is a constant-elasticity Cobb-Douglas production function. ↑

- Bureau of Labor Statistics, “Occupational Employment Statistics,” available at: https://www.bls.gov/oes/tables.htm. ↑

- Institute for Energy Research, “The Hidden Costs of Wind Power,” January 4, 2013, website, http://instituteforenergyresearch.org/analysis/the-hidden-costs-of-wind-power/. ↑

- Rich, Howard, “Germany’s Green Energy Disaster: A Cautionary Tale for World Leaders,” Forbes, March 14, 2013, http://www.forbes.com/sites/realspin/2013/03/14/germanys-green-energy-disaster-a-cautionary-tale-for-world-leaders/#3fdb66b814a6Martin, Richard, “Germany Runs Up Against the Limits of Renewables,” MIT Technology Review, May 24, 2016, https://www.technologyreview.com/s/601514/germany-runs-up-against-the-limits-of-renewables/. ↑

- Incentive Evaluation Commission, Tax Incentive Evaluation Report 2016, pdf page 157. ↑

- Ibid, pdf page 264. ↑

- “U.S. Tax Incentive Info,” website, Film Producation Capital, http://www.filmproductioncapital.com/taxincentive.html. ↑

- Verrier, Richard, “Are Film Tax Credits Cost Effective?” Los Angeles Times, August 30, 2014, http://www.latimes.com/entertainment/envelope/cotown/la-et-ct-fi-film-tax-credits-20140831-story.html. ↑

- Even the IEC’s recommendation to end wind energy credits, which significantly impact the state budget, carries little value given the general consensus already building that something needed to be done. ↑